Anduril Is Real. The Price Isn't.

The Founder Nobody Was Supposed to Hire

In 2016, Palmer Luckey was the most celebrated twenty-something in Silicon Valley. He had built Oculus VR in his parents’ trailer, sold it to Facebook for $2 billion at age 21, and was on the cover of Time magazine wearing a VR headset while floating mid-air. He was the face of the next platform shift.

Then it emerged he had donated $10,000 to a pro-Trump internet group during the presidential campaign. In March 2017, Facebook parted ways with him. He was 24. He has said publicly he would not have left otherwise; Facebook said the departure was unrelated to his politics.

Most founders in that position would have retreated into angel investing or a quieter second act. Luckey did the opposite. He founded Anduril Industries, named after the sword reforged from the shards of Narsil in Tolkien’s Lord of the Rings, and set out to rebuild the American defense industrial base from scratch. The pitch was simple and confrontational: the traditional defense primes (Lockheed, Raytheon, Boeing, Northrop) were slow, bureaucratic cost-plus contractors that charged the government enormous sums to build mediocre systems over a decade. Silicon Valley could do it better, faster, and cheaper by self-funding R&D and selling finished products.

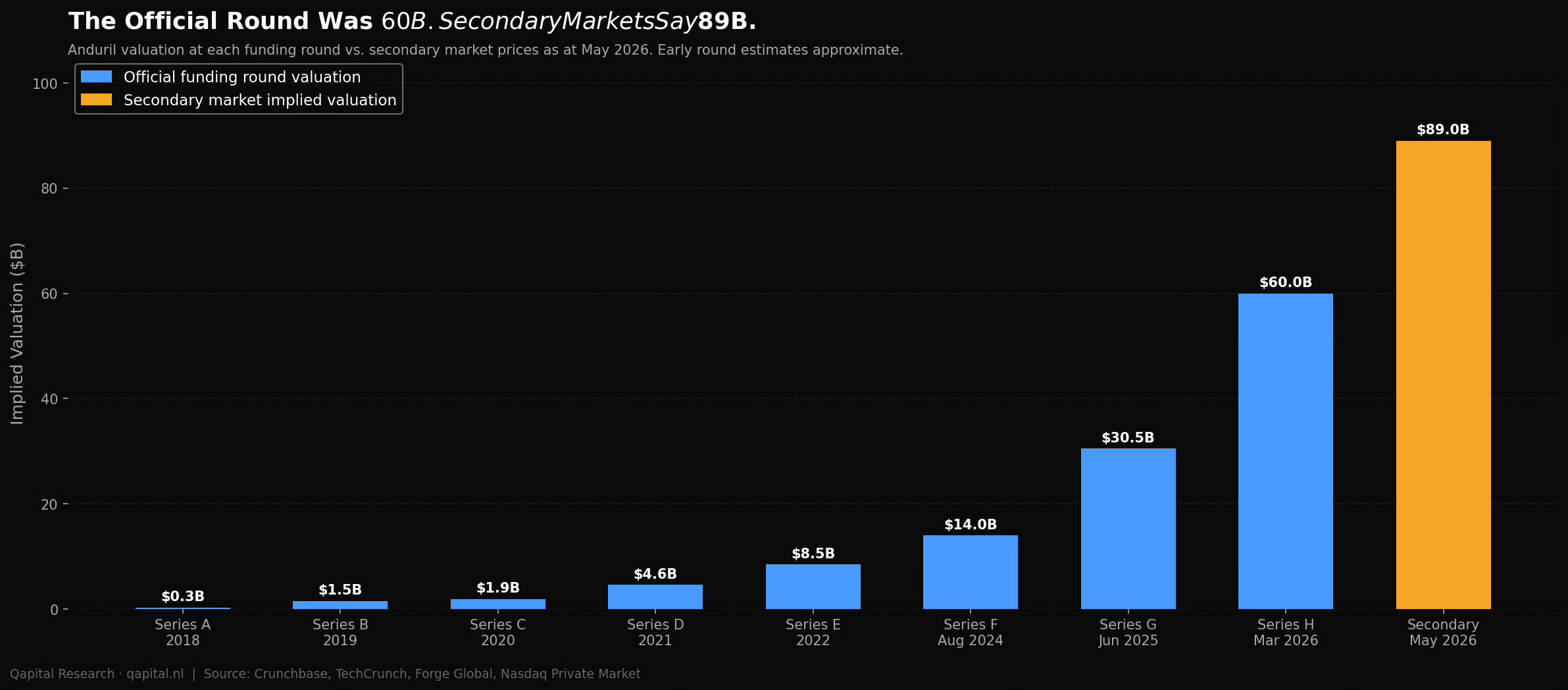

Eight years later, Reuters reports Anduril reached $2.2 billion in 2025 revenue and closed a round valuing it at $61 billion. It took over Microsoft’s role in the IVAS program, originally tied to a potential $21.9 billion Army contract, and is building a reported five-million-square-foot autonomous weapons factory in Ohio. On secondary markets, reported trades have implied a valuation around $89 billion, roughly three times the Series G price set less than a year ago.

The business is remarkable on its own terms. The price at which people are buying it in the secondary market is a different question entirely.

The Sovereign Customer Illusion

Every exceptional company generates a specific cognitive bias in its investors. For Palantir, it was the Exception Reflex: valuation skepticism feels like a failure of imagination when the business is this good. For Anduril, the bias is different in character and more seductive in form.

Call it the Sovereign Customer Illusion: the belief that having the United States Department of Defense as your primary customer eliminates commercial downside risk. When the buyer is the most powerful government on earth and the product is national security, normal financial analysis begins to feel beside the point. Who models a bear case on the company protecting the southern border? Who stress-tests contract renewal probability when the product is keeping soldiers alive?

The Illusion has several layers. First, it conflates mission criticality with contract certainty. The DoD needs autonomous systems; it does not necessarily need Anduril’s autonomous systems at any given contract renewal. Second, it treats government spending as stable when Anduril’s own political environment makes it anything but: the company’s closest political allies are running an explicit government efficiency agenda. Third, it assumes that early contract wins represent durable competitive position, when the defense procurement process is specifically designed to maintain competitive pressure over time.

The Sovereign Customer Illusion does not mean Anduril is a bad business. It means the bias leads investors to apply a lower return requirement, and therefore a higher valuation multiple, than the actual risk profile justifies. Understanding the Illusion is the entry point for a clear-eyed view of what Anduril is actually worth.

The Man and the Factory

Palmer Luckey is unlike most defense company founders in the same way that he was unlike most VR founders: he understands the systems he builds at a component level, not just the business around them. He taught himself electronics as a teenager, built his first VR headset prototype at 18, and has described designing weapons systems with the same technical curiosity he brought to consumer hardware. The forward-deployed engineers that Anduril embeds with military units were his idea: send the builders to where the weapons are used, not the users to Silicon Valley.

His political history is relevant in ways that go beyond biography. JD Vance, now Vice President, was an Anduril investor before his political career. Peter Thiel’s Founders Fund has led or participated in virtually every Anduril funding round, committing $1 billion in the Series G alone. Trae Stephens, a Founders Fund partner, serves as Anduril’s chairman. The company’s political network and its investor base overlap to a degree unusual even by Silicon Valley standards.

This creates a structural feature that cuts both ways. The current administration’s priorities, border security, autonomous warfare, and reducing dependence on traditional primes, align almost exactly with Anduril’s product portfolio. The southern border surveillance contract alone is a $2 billion IDIQ with approximately $818 million already obligated. The IVAS program, originally tied to a potential $21.9 billion Army contract and transferred from Microsoft to Anduril in February 2025, fits directly into the Army’s soldier-worn computing roadmap. The follow-on SBMC phase is now competitive, with Anduril and Rivet both receiving prototype awards.

The risk is that political alignment is not a moat. A different administration, a different set of priorities, or simply a different set of procurement officers can redirect contract flow without breaking any rule. Anduril’s closest political relationships are assets today. They are also concentration risk.

Then there is Arsenal-1.

The factory is the central bet of the Anduril investment thesis. Not Lattice OS, not the contract portfolio, not the growth rate. The factory. Arsenal-1 is a $1 billion, five-million-square-foot autonomous weapons manufacturing facility under construction in Columbus, Ohio, targeting production start in July 2026. It is intended to manufacture Anduril’s hardware systems: drones, counter-drone systems, autonomous air vehicles. The target is a scale and cost structure no defense prime has achieved with modern methods. First production is targeted for July 2026; the facility remains under construction.

No Silicon Valley company has attempted prime-level defense manufacturing at this scale before. Aerospace and defense manufacturing is not software. Quality control failures produce real-world consequences. Unit economics on weapons systems depend on supply chain discipline that takes years to develop. The companies that have tried to transfer commercial manufacturing principles to defense programs, and there are several, have mostly learned that the analogy breaks down at scale.

Arsenal-1 is either the moment Anduril proves the thesis or the moment the thesis meets reality. The secondary market is pricing in the former.

What Lattice Actually Does

The right mental model for Anduril is not a defense contractor. It is not quite a software company either. It is a defense operating system company that also manufactures the hardware that runs on it.

Lattice OS is the core asset. It is an AI software platform that fuses data from thousands of sources: drones, surveillance towers, satellite feeds, ground sensors. The output is a real-time, three-dimensional operational picture. Lattice processes this data, identifies threats, and directs responses: autonomous systems respond to Lattice commands under human supervision. The platform is exposed via an open SDK with REST and gRPC APIs, allowing third-party sensors and platforms to integrate. In architecture terms, Lattice is attempting to be the iOS of autonomous warfare: the layer that everything else runs on top of.

The commercial model built around Lattice is structurally different from how traditional defense works. Legacy primes wait for government RFPs, bid on cost-plus contracts, and spend taxpayer money on R&D. They are incentivised to extend programs and increase costs. Anduril self-funds product development, builds finished systems, and sells them at fixed prices. This is why analyst estimates put Anduril’s gross margins in the 40-45% range, versus the 8-10% typical of traditional primes. Anduril does not publish financials, so these figures are analyst extrapolations from contract economics and company positioning. When you build the product before the government buys it, you capture the development margin.

The hardware portfolio built on Lattice includes: Roadrunner-M, an autonomous air vehicle with over $350 million in orders including a 500-unit package; the Dive-LD autonomous underwater vehicle; Autonomous Surveillance Towers deployed along the southern border; Fury, an autonomous combat aircraft; and the Anvil counter-drone system. IVAS, the $22 billion Army AR headset program, is the newest addition and the most complex by an order of magnitude, combining Lattice’s computer vision with physical hardware that soldiers wear in combat.

The Lattice licensing model matters for the valuation. Every deployed drone, tower, or underwater robot running Lattice pays a software license. As the hardware portfolio scales, the software revenue compounds underneath it. This is the bull thesis: Anduril is building a recurring revenue base while also selling high-margin hardware. The combination is structurally more valuable than either business alone.

What this model requires is that Arsenal-1 produces hardware at scale, reliably, on cost. Everything else follows from that.

The Competition Nobody Talks About Directly

Anduril is often positioned against the traditional defense primes: Lockheed Martin, Raytheon, Boeing, Northrop Grumman. This framing is convenient for Anduril’s narrative but understates the actual competitive picture.

The primes are slow and they know it. Every major prime has an innovation lab, a venture arm, and a set of internal programs designed to import Silicon Valley speed. They are not sitting still. More importantly, they have something Anduril does not: decades of cleared manufacturing facilities, supply chain relationships, and program management experience with systems that actually go to war. When Arsenal-1 opens, Anduril will be competing with companies that have been building weapons in volume for fifty years.

The more direct competition is the peer class: other defense tech startups that have attracted serious capital on similar theses. Shield AI, which builds AI pilots for military aircraft operating in GPS-denied environments, reached a $12.7 billion valuation in March 2026 after a $2 billion raise. Shield AI’s V-BAT drones have seen real battlefield deployment in Ukraine, generating the kind of combat-validated data that Anduril’s systems have not yet accumulated at the same scale. At $12.7 billion on roughly $300 million in reported revenue, Shield AI trades at a higher revenue multiple than Anduril, though at a fraction of the absolute size.

The most interesting competitor is not a startup. Microsoft could not make IVAS work. It spent years and hundreds of millions on the AR headset program before Anduril took over in February 2025. That is evidence of Anduril’s capability: the Army chose them over one of the most resourced technology companies on earth. It is also a warning about what the program requires. AR hardware that functions in combat environments, integrates with Lattice’s computer vision, and survives the US Army’s qualification process is hard in ways that no software background prepares you for. Microsoft, with substantial resources, struggled to deliver a viable system. The fact that Anduril has taken it on is admirable. The fact that it represents a significant share of the long-term contract value is a concentration risk.

The Numbers Behind the Narrative

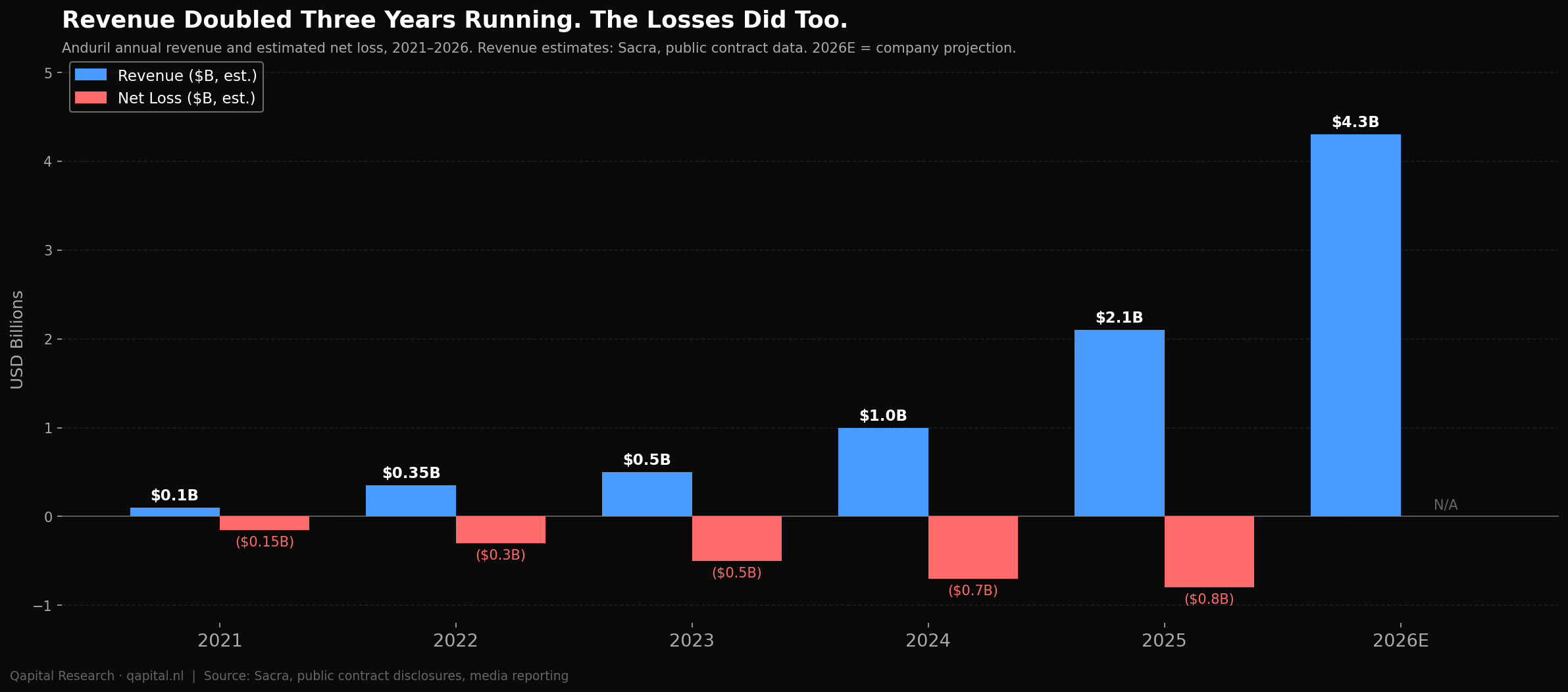

The financial picture of a private company growing at 110% annually while reporting losses exceeding $1 billion per year requires careful reading. There are no audited public filings. The revenue and loss figures come from Reuters, The Information, and media reporting based on contract data. The structure of those losses matters as much as the size.

The revenue trajectory is real and accelerating. From roughly $100 million in 2021 to $1 billion in 2024, Reuters reported 2025 revenue of $2.2 billion. The Information reported in March 2026 that Anduril was projecting $4.3 billion for 2026, which if achieved would represent a doubling of revenue for the third consecutive year. Analyst estimates place gross margins in the 40-45% range, though this is extrapolation rather than disclosed fact.

The losses are a different kind of signal. The Information reported losses exceeding $1 billion annually, driven by Arsenal-1 construction, IVAS integration, Fury development, and Lattice platform extension. These are not operational losses from an inefficient business. They are pre-revenue-recognition outlays on contracts that will generate revenue when milestones are hit. The structure is closer to a construction company booking revenue on completion than to a software company with a cost problem.

What this means is that the path to profitability runs directly through Arsenal-1. When the factory produces at planned capacity, the hardware revenue recognises against the invested cost, and the margin structure of the business becomes clear. Until that happens, the loss is a placeholder for an outcome, not a verdict on one.

Two numbers capture the valuation tension. At the Reuters-reported valuation of $61 billion on $4.3 billion of projected 2026 revenue, Anduril trades at roughly 14 times forward revenue. Lockheed Martin trades at 1.7 times revenue. Raytheon trades at 2.1 times. The premium Anduril commands over the traditional primes reflects its growth rate, its commercial model, and the software layer underneath the hardware, and that premium is arguably justified at the official round price. Fourteen times revenue for a business growing this fast is defensible if Arsenal-1 works.

The secondary market is a different story. Reported trades on platforms like Forge and Nasdaq Private Market have implied a valuation around $89 billion, roughly 21 times projected 2026 revenue. Secondary markets in private companies are thin and not always representative of true clearing prices, but the direction of travel is clear: the gap between official round pricing and secondary implied value has widened sharply in a short window. FOMO has entered the building, and it arrived fast.

Arsenal-1 and the Reliability Problem

The central analytical question for Anduril is not whether Lattice is differentiated or whether defense tech is a good sector to invest in. It is whether a Silicon Valley company can actually manufacture weapons at prime-level scale, reliably and on cost, for the first time in history.

The early evidence is mixed in ways that deserve more attention than they receive in bull-case analyses.

The Wall Street Journal and Reuters reported in late 2025 on a series of setbacks across Anduril’s product lines. A ground test of Fury, Anduril’s autonomous combat aircraft, reportedly resulted in a mechanical failure that damaged the engine ahead of a critical Air Force evaluation. Separately, a test of the Anvil counter-drone system was reported to have caused a wildfire in Oregon; the exact acreage varies across sources. Anduril’s response was that these represent a “tiny fraction” of tests, which may be true. The issue is not the fraction. The issue is that weapons that fail in testing fail in the field, and the Army, Navy, and Air Force qualify systems through rigorous testing precisely because the cost of a field failure is measured in lives, not write-downs.

These incidents do not make Anduril a bad investment. They do make Arsenal-1 a binary bet. If the factory opens on schedule in July 2026, hits production targets, and the systems it produces pass qualification, the thesis accelerates. If production lines stall, quality control fails, or the government delays acceptance of systems that haven’t cleared testing, the valuation model built on $4.3 billion of 2026 revenue becomes untenable quickly.

The history of defense manufacturing scale-ups is not encouraging. Every major defense program in recent history: the F-35, the Littoral Combat Ship, the Future Combat Systems, the original IVAS. Each has experienced cost overruns and schedule slippage. The standard answer is that Anduril’s commercial model avoids the perverse incentives of cost-plus contracting. That is true. It does not follow that self-funded commercial development produces hardware that works in military environments on the first cycle.

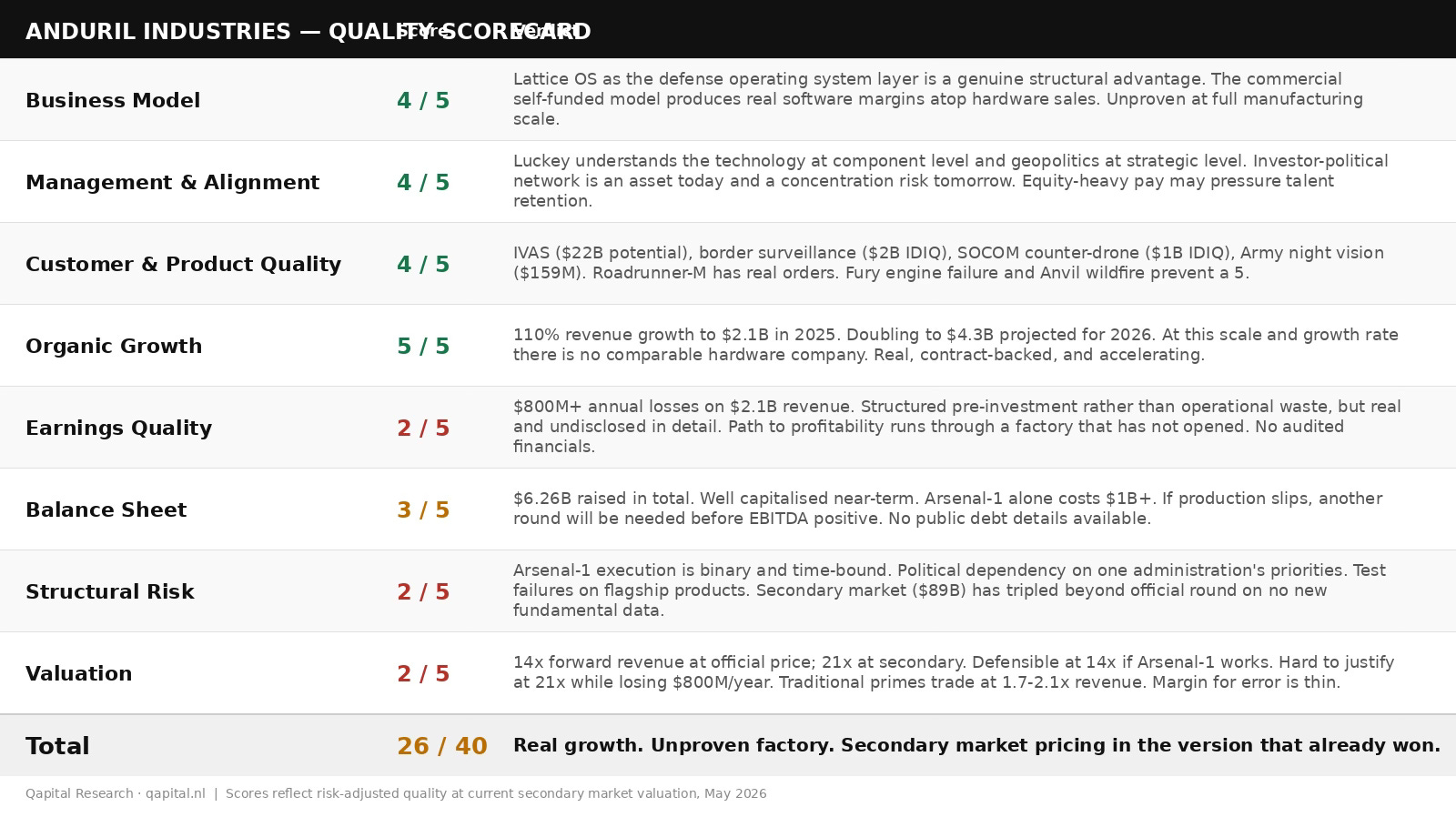

The Quality Scorecard

Eight dimensions. Each scored 1-5.

Overall: 26 / 40

The top four dimensions: growth, business model, management, and customer quality. All strong. The bottom four: losses, structural risk, and valuation. These reflect a company asking investors to pay for a future that requires multiple simultaneous things to go right. The scorecard is not a verdict on the business. It is a verdict on the risk-adjusted price at which that business is currently available.

Building a Fair Value

Valuing a private company that does not publish financials requires a different discipline than valuing a listed one. The inputs are less precise. The range of outcomes is wider. The discipline required is the same: anchor to what can be known, stress-test the assumptions, and resist the pull of the narrative.

Here is what can be known. Revenue of $2.2 billion in 2025, reported by Reuters. A 2026 projection of $4.3 billion, reported by The Information. Estimated gross margins of 40-45%, based on analyst extrapolation rather than disclosed filings. A $1 billion factory that either opens in July 2026 or doesn’t. A contract potentially worth up to $22 billion that either scales or doesn’t. Reported secondary market trades implying a valuation around $89 billion, which is more than Northrop Grumman.

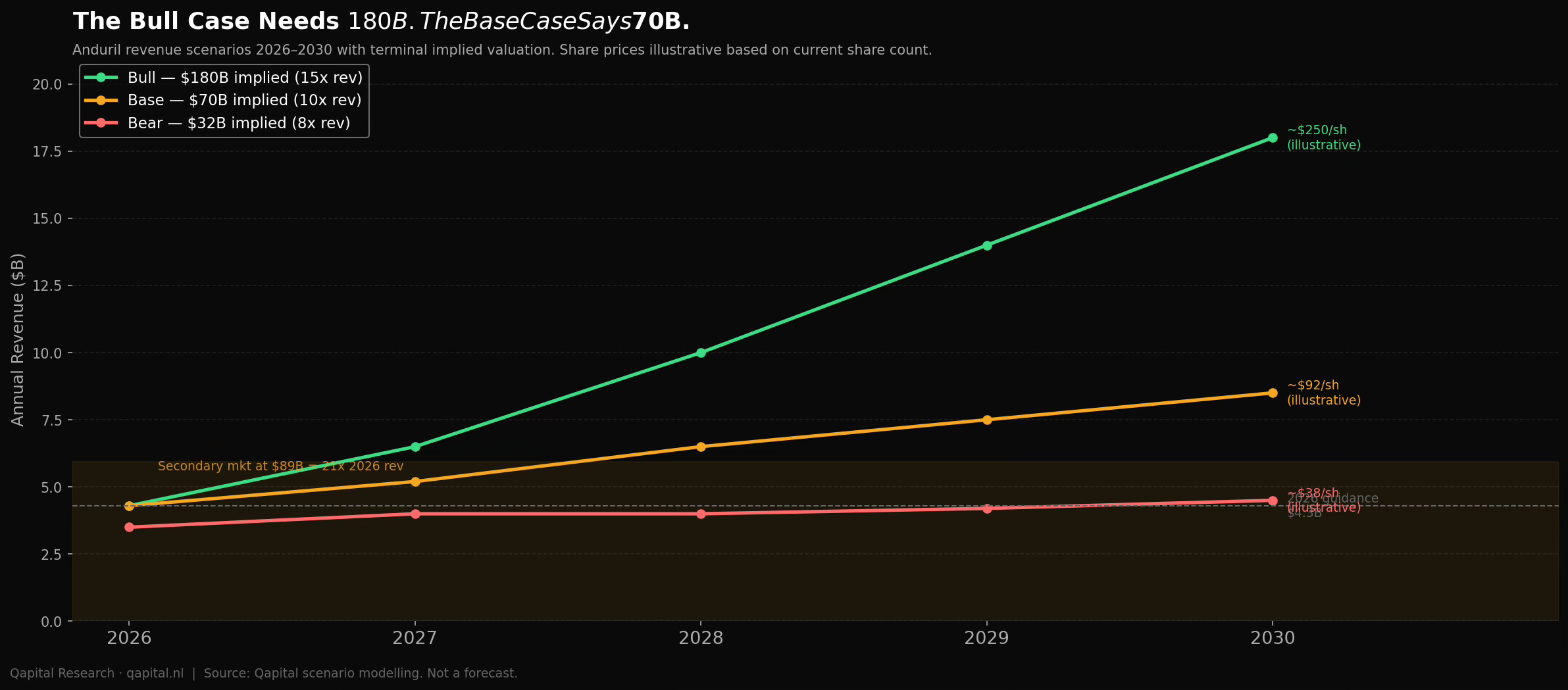

Bull case: Arsenal-1 opens on schedule. Fury passes Air Force qualification. IVAS scales to full program value. Revenue reaches $12 billion by 2028 as hardware production accelerates, Lattice licensing compounds, and international customers begin buying. GAAP profitability arrives in 2027 as manufacturing margins normalize. At 15 times 2028 revenue of $12 billion, the company is worth $180 billion at IPO. At current share count, the secondary market at $89 billion is still cheap. The bull case requires everything going right simultaneously.

Base case: Arsenal-1 opens with some slippage, six to twelve months late and over initial budget. Fury qualification takes longer than expected. IVAS proves the hardest program Anduril has attempted and scales at half the pace projected. Revenue reaches $6-7 billion by 2028. Losses persist through 2027. IPO happens at 10 times 2028 revenue of $7 billion, implying $70 billion. The secondary market at $89 billion is modestly overpriced. The official round at $60 billion roughly reflects fair value.

Bear case: Arsenal-1 experiences significant production issues in its first year. A major contract, IVAS or a border surveillance renewal, faces delays or restructuring tied to political or budgetary shifts. Growth slows to 40% by 2027 as near-term contract tailwinds subside. Revenue reaches $4 billion by 2028. Losses widen as fixed manufacturing costs scale faster than revenue. IPO either delays to 2028 or prices at a significant discount to current rounds. At 8 times revenue of $4 billion, the company is worth $32 billion, which is 64% below the secondary market price today.

The base case implies the reported round valuation ($61 billion) is roughly fair. Reported secondary market pricing around $89 billion appears to sit between the base and bull case, with no additional risk premium for Arsenal-1 uncertainty. The bear case implies that secondary market buyers at today’s prices have paid twice what they should have.

The reverse question is equally clarifying: what does Anduril need to be worth for a secondary market buyer at the implied $89 billion to earn 10% annually over five years? The company would need to be worth approximately $143 billion in 2031. At a reasonable 12 times revenue on a scaled defense technology business, that requires $12 billion of revenue by 2031, roughly a 4x increase from the 2026 projection, compounded annually at around 23% per year, for five years, from a company that has never manufactured at scale and is currently reporting losses exceeding $1 billion annually.

That is achievable. It is not the base case.

The Bold Call

Palmer Luckey built something that almost no one in Silicon Valley believed could be built. He took the defense prime model apart, funded his own R&D, built real products that real militaries are deploying, and reached $2.2 billion in reported 2025 revenue eight years after founding. The Lattice platform is differentiated in a way that matters: no traditional prime has built anything close to it. The commercial model produces margins that Lockheed’s cost accountants cannot explain. The IVAS contract is either the defining win of a generation-defining company, or the hardest thing Anduril has ever attempted.

Here is what the bull case would need to be true: Arsenal-1 opens on time and reaches production targets in its first operating year. Fury passes Air Force qualification without further test failures. IVAS scales successfully where Microsoft, with ten times the resources, could not. International customers begin buying in volume, extending the TAM beyond US government dependency. Anduril reaches profitability before it needs another funding round.

None of those things have happened yet.

What would change this rating: Arsenal-1 running at planned capacity with validated unit economics. IVAS completing a successful fielding phase. Two consecutive quarters of narrowing losses. An IPO priced at or near the latest reported round valuation of $61 billion.

Our rating: AVOID.

Not the business. The price. The reported $61 billion round is a number a disciplined analyst can engage with seriously. Reported secondary market trades implying $89 billion are a number built on momentum, narrative, and the fear of missing something historic. At $89 billion, the implied valuation is roughly 21x projected 2026 revenue and more than 40x reported 2025 revenue. With losses reported to exceed $1 billion annually and a factory that has not yet produced a single unit at scale, the risk-reward is negative. The base case implies roughly 21% downside from secondary implied prices. The bear case implies 64%.

If the IPO prices at or near $61 billion, come back and look again. Until then: the factory has to prove itself first.

This article is for informational purposes only and does not constitute investment advice. All figures in USD unless noted. Revenue reported by Reuters (May 2026); losses reported by The Information (March 2026); valuation from Reuters. Secondary market pricing based on reported trades on Forge and Nasdaq Private Market, which are thin markets and may not reflect true clearing prices. Anduril does not publish audited financials. Margins are analyst estimates. Scenarios are illustrative and should not be treated as forecasts.