AppLovin: The Platform in the Wrong Costume

The Ad Machine Nobody Believes

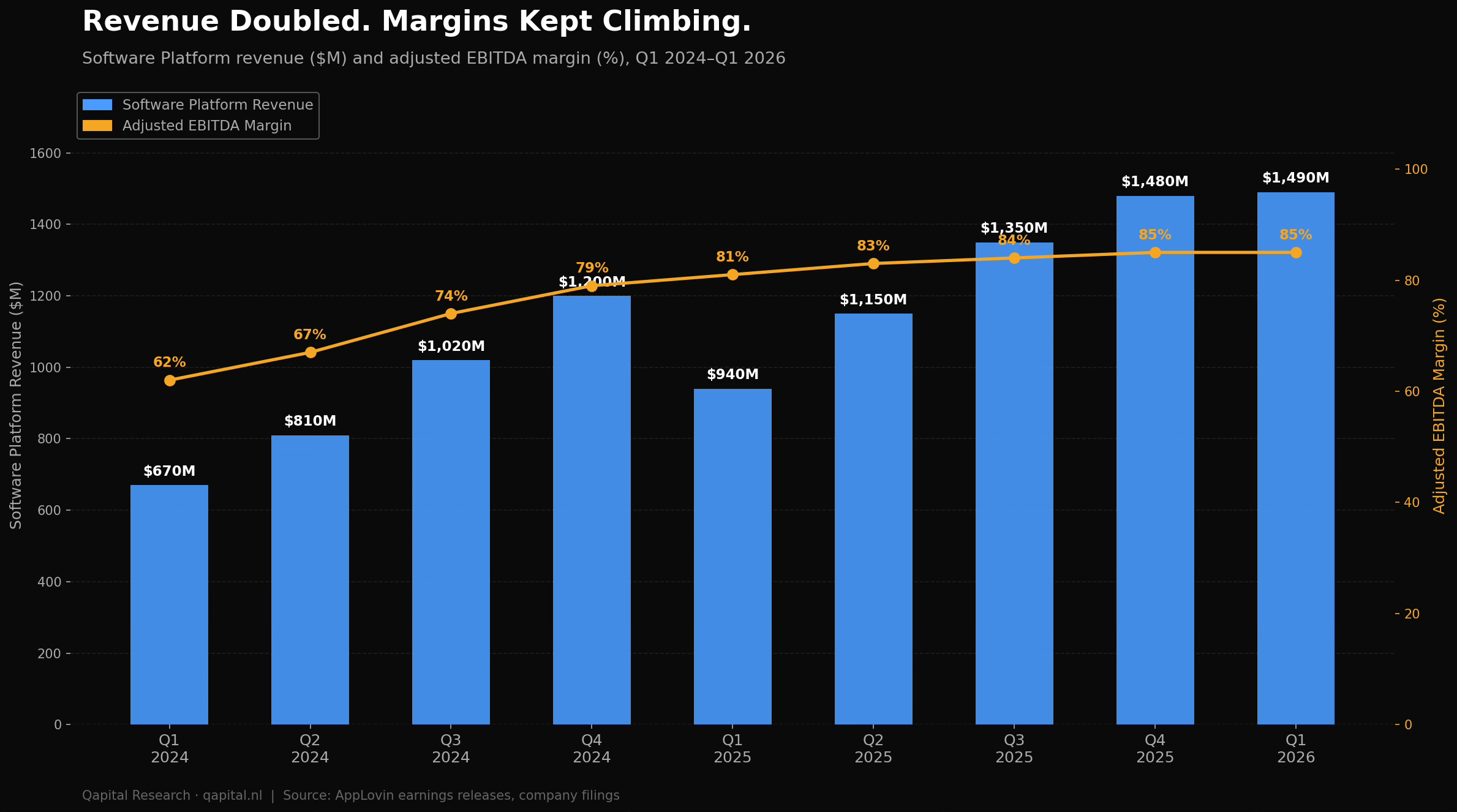

AppLovin Corporation reported Q1 2026 results on May 7, 2026. Revenue grew 59% year-over-year to $1.84 billion. The software platform produced an 85% EBITDA margin on $1.49 billion in segment revenue. Free cash flow was $1.29 billion in three months. The company raised full-year guidance and beat analyst estimates on every metric that mattered.

The stock is down approximately 37% from its all-time high.

A company growing at 59% with 85% operating margins, generating run-rate free cash flow tracking above $4 billion annually, trades at approximately 35% below its 52-week high of $745. The market knows AppLovin sold its games. It has not fully decided what that makes the business worth.

In 2021, when AppLovin went public, it was a mobile gaming and app advertising company. It owned a portfolio of mobile games, ran an ad network called AppDiscovery, and competed in a market that most analysts classified as ad-tech. Ad-tech companies trade at 5x to 10x EBITDA. Gaming companies trade at 10x to 15x earnings on a good day.

In 2024, AppLovin sold its entire games portfolio to focus exclusively on its software platform. The games are gone. The label is not.

That label is doing a lot of damage to the price.

Category Drag

Every mispriced company has a specific mechanism driving the mispricing. For Palantir, it was the Exception Reflex: valuation skepticism felt like a failure of imagination when the business is that good. For Anduril, it was the Sovereign Customer Illusion: the US government as primary customer appeared to eliminate the downside case in investors’ minds.

For AppLovin, the mechanism is Category Drag.

Category Drag occurs when the market assigns a multiple based on what a company used to be rather than what it currently is. The category becomes the lens. New facts that contradict the category are processed as exceptions rather than evidence of reclassification. The multiple barely moves.

AppLovin’s Category Drag runs like this. The company IPO’d as a gaming and ad-tech business. Both segments attract low multiples: gaming because growth is slow and cyclical, ad-tech because margins are thin and advertiser concentration is high. The market set its model accordingly. Then AppLovin’s AI recommendation engine, AXON 2.0, began producing return-on-ad-spend numbers that outperformed every competing platform in mobile app install advertising. The software platform grew from a useful tool into the dominant infrastructure in its category. Margins expanded from around 50% to 85%. The games business was sold. The company became, in economic substance, a pure-play AI advertising platform.

The multiple reflects partial reclassification, but still embeds a meaningful probability discount on whether current economics are durable. The market is not unaware of the software shift. It assigns a probability to the possibility that the 85% margins are overstated, that the SEC investigation produces a material finding, or that AXON’s edge does not port outside gaming. The question is not whether investors have read the press releases. The question is whether the probability discount is too large relative to the evidence.

Category Drag affects both buyers and sellers. Bears anchor on the gaming origin story and an open SEC inquiry to justify the lower multiple. Bulls have at points overcorrected, pricing perfection without accounting for real structural risks. The mispricing lives in the gap between those two reflexes. Neither camp has reclassified cleanly.

The right frame is neither. AppLovin’s software platform is a specific kind of business: a two-sided marketplace intermediating between app publishers and advertisers, powered by an AI recommendation engine that improves with scale. That business, assessed against the peer set it now resembles, trades at a discount. The discount may be rational given the open risks. The question is whether it is too large.

The discount is the opportunity.

The Builder and the Algorithm

Adam Foroughi is not a typical software company CEO. He is not a trained engineer, a former consultant, or a second-time founder working from a playbook. He is a self-taught programmer who built and sold several small companies before co-founding AppLovin in 2012 with John Krystynak and licensed attorney Andrew Karam.

His founding insight was specific and operational: mobile app developers were producing good products but had no efficient way to find and acquire users at scale. The app stores provided discovery but not targeting. Advertising networks existed but performed poorly on conversion metrics. Foroughi believed the right recommendation engine could change this. He built AppDiscovery, AppLovin’s core ad product, to prove it.

The bet on AXON 2.0 was Foroughi’s personal call. In investor communications, he has described building the AI capability from the ground up rather than integrating third-party models. The performance gap between AXON 2.0 and competing platforms, which became visible in advertiser return-on-ad-spend metrics starting in late 2023, is the output of that decision. Management and large gaming advertisers have publicly described ROAS improvements that were material enough to shift budget allocation at scale. AppLovin’s software revenue growing at 59% while the overall mobile gaming market was flat is the disclosed outcome. Budget follows performance. That is what the numbers show.

Foroughi owns approximately 14% of AppLovin’s outstanding shares. He has not been a consistent net seller at elevated prices, which is notable for a founder sitting on a concentrated position at current valuations. The co-founders remain in operational roles. CFO Herald Chen, who came from KKR’s private equity operation, has been with the company since 2020 and brings a financial discipline to capital allocation that is visible in the FCF conversion numbers.

The governance structure is unusual in one respect: Foroughi and the founding team hold Class B shares with elevated voting rights, concentrating effective control despite the public float. This is founder-controlled in substance. It limits the risk of a board removing a capable CEO during a growth cycle, which matters because AppLovin’s most important years are likely ahead of it.

The risk of founder control at a company with this momentum is not misalignment; the equity ownership makes that largely self-correcting. The risk is strategic rigidity: a founder so committed to AXON’s thesis that correction signals take longer to reach the decision layer than they should. That risk cannot be quantified from the outside. It exists.

What AXON Actually Does

The mental model most investors use for AppLovin is wrong. It is not a mobile ad network. It is not a gaming holding company. It is a real-time recommendation engine that intermediates between supply, mobile app publishers showing ads, and demand, advertisers wanting to reach mobile users, and earns a margin on the spread between what advertisers pay and what publishers receive.

AXON 2.0 is the intelligence layer. It processes signal from across AppLovin’s publisher network, which covers billions of monthly active users across tens of thousands of apps, and predicts in real time which ad to show which user at what price. The prediction is not generic. It is calibrated to the specific outcome the advertiser cares about: an app install, a purchase, a subscription. AXON bids on each impression accordingly.

The flywheel is structural. More publishers joining the network produce more behavioral signal. More signal makes AXON’s predictions more accurate. More accurate predictions produce better results for advertisers. Better results attract more advertiser spend. More spend makes the network more valuable to publishers. The loop reinforces itself in both directions.

AppLovin’s MAX mediation product adds a second layer. MAX is a header bidding platform: it allows publishers to run their AppLovin inventory alongside other demand sources, including Meta and Google, in a single unified auction. AppLovin earns a fee for operating the auction infrastructure. This is a structurally sticky product. Switching mediation platforms is technically complex and operationally risky for publishers whose business models depend on reliable ad revenue.

The e-commerce expansion is the next chapter. AXON was built on mobile gaming advertiser data. In 2025, AppLovin began opening the platform to e-commerce and direct-to-consumer brands. The logic is sound: e-commerce brands need mobile performance advertising at scale, and AXON’s prediction infrastructure is not inherently category-specific. The TAM expansion from mobile gaming app installs to general performance commerce is significant on paper.

The Q1 2026 results include early e-commerce contribution. Management noted the vertical as a growing contributor in the earnings call without breaking out the segment separately. The failure mode is that AXON’s signal advantage may be specific to in-app gaming environments. In-app gaming signal lives inside AppLovin’s own publisher network, where the company controls the data. E-commerce signal is fragmented: it lives across Shopify storefronts, Meta pixels, Google Shopping feeds, and transaction records that AppLovin cannot access. These are structurally different assets. A model trained on the first may not transfer cleanly to the second. If AXON’s edge is gaming-specific, the e-commerce expansion will disappoint.

That question is open. It is the most important open question in the AppLovin investment thesis.

The Google Comparison Nobody Makes Correctly

The standard competitive framing puts AppLovin against other mobile ad platforms: Google’s UAC (Universal App Campaigns), Meta’s Advantage+, and Unity’s LevelPlay. This framing is partially accurate but misses the more important structural point.

Google and Meta are AppLovin’s competitors. At the budget allocation level, the competition is direct: a dollar going to AppLovin’s AppDiscovery is a dollar not going to Google UAC or Meta Advantage+. Advertisers choose. The more useful question is not whether they compete but where each platform wins, because the answer shapes the ceiling on AppLovin’s addressable market.

Google UAC dominates mobile app install advertising by total budget. It uses first-party search and Play Store signal to target app installers, benefiting from purchase-intent data that AppLovin does not have access to. Meta Advantage+ uses social graph and behavioral data from Facebook and Instagram, strong for reach and upper-funnel discovery. Neither platform has access to the in-app behavioral signal that AppLovin’s publisher network provides.

AppLovin’s specific edge is in-app signal. When a user is actively playing a mobile game, AppLovin knows their engagement depth, their in-app purchase behavior, their session patterns, and their responsiveness to specific ad formats. This behavioral data does not exist in Google or Meta’s systems. For advertisers whose target user is an active mobile gamer, AXON’s signal is better. That is a narrow moat on a specific population. It is also a real one.

The constraint is that mobile gaming is not growing as a category. Global mobile gaming revenue has been roughly flat for two years, affected by Apple’s App Tracking Transparency changes from 2021 and a broader maturation of the market. AppLovin has grown inside a flat category by taking share from competitors. That is impressive. It also means the ceiling is the category itself unless the e-commerce expansion unlocks new TAM.

Unity, the most relevant direct competitor on the mediation side, is in operational disarray. Its LevelPlay mediation platform is market-relevant, but Unity’s financial position and management instability have made it a less reliable partner for publishers. AppLovin has taken mediation share from Unity consistently over the past two years. That tailwind may have a limited remaining runway as the share transfer approaches completion.

There is a structural risk this section cannot leave out. AppLovin’s entire signal advantage depends on access to in-app behavioral data, and that access is contingent on platform policy set by Apple and Google. Apple’s App Tracking Transparency framework, introduced in 2021, was the last major disruption: it restricted cross-app tracking and damaged every ad platform that relied on IDFA-based targeting. AppLovin adapted by leaning harder into the in-app signal it controls directly, which is what made AXON 2.0 work. But Apple and Google each control the environment in which AppLovin’s publisher network operates. A further restriction on in-app data collection, or a change to how third-party ad networks can operate inside native apps, would hit AXON’s signal layer directly. This risk has no hedge and no visible mitigation. It is not imminent. It is real.

The honest competitive summary: AppLovin is the best-performing platform in a specific and defensible segment, taking share from a weakened competitor, with a plausible but unproven expansion into adjacent markets, and a structural dependency on Apple and Google that it cannot control. At approximately 26x next-twelve-months EBITDA, that is not a bad position to be in.

Three Numbers You Need

AppLovin’s financial profile looks like a software business, not an ad-tech business. This is the core of the Category Drag thesis, and the numbers support it directly.

Revenue in Q1 2026 was $1.84 billion, up 59% from $1.16 billion in Q1 2025. The software platform accounted for $1.49 billion of that. EBITDA on the software platform was approximately $1.27 billion, an 85% margin. That figure is segment-level EBITDA as AppLovin defines it: certain shared infrastructure and corporate costs are allocated outside the segment. The fully-loaded GAAP operating margin is closer to 72%, which is the cleaner reference for cross-company comparison. Both numbers are exceptional. For context, Alphabet’s Google advertising segment runs at around 35% operating margins. Meta’s advertising business runs at roughly 45%. Even at 72%, AppLovin’s software platform is a different category of economics.

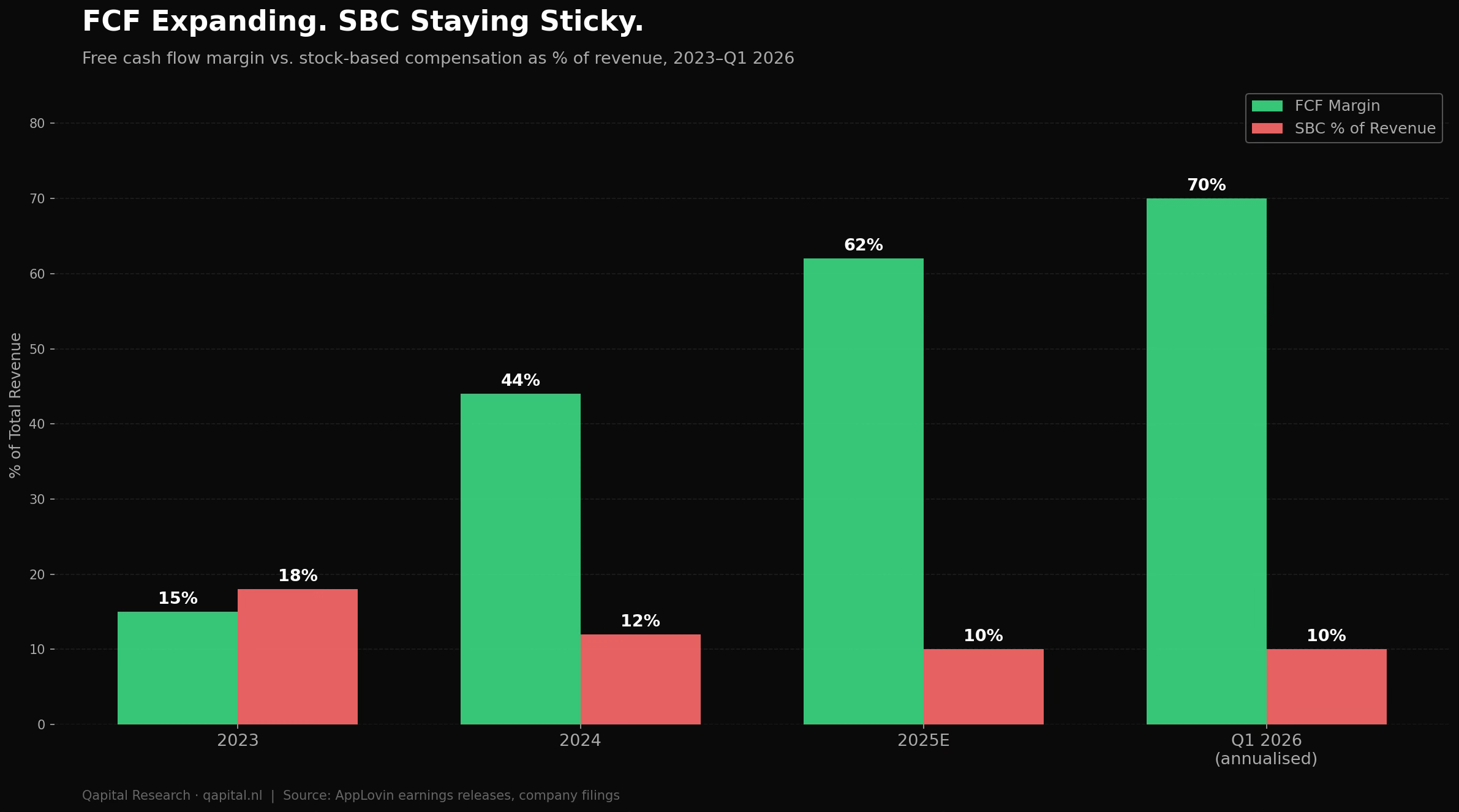

Free cash flow was $1.29 billion in the quarter. AppLovin’s FCF can vary meaningfully between quarters due to advertiser prepayment timing and working capital effects, so a single quarter is not the right anchor. The trailing run rate, taking the last several quarters together, tracks above $4 billion annually. The stock at approximately $482 implies a market capitalization around $167 billion and an enterprise value, after accounting for net debt, of roughly $171 billion. At $4 to $5 billion run-rate FCF, the business trades at approximately 34x to 43x free cash flow, depending on the period used. For a company growing FCF at 59%, that is not a distressed valuation, but it is not cheap either.

The balance sheet carries net debt of approximately $3.5 billion, a legacy of the capital structure built during the acquisition years when AppLovin was assembling its gaming portfolio. The debt is manageable at current EBITDA levels: net leverage is below 1x trailing EBITDA. It is not a pressing concern. It is worth noting because it means the company cannot deploy share buybacks at scale simultaneously with debt service when something unexpected happens.

Stock-based compensation ran at approximately $180 million in Q1 2026, roughly 10% of GAAP revenue and around 14% of EBITDA. This is higher than is comfortable for a company claiming exceptional margin performance. It also partly explains why the market does not fully trust the 85% headline: a platform with software-grade economics at maturity should not require this level of SBC to retain talent. That suspicion is embedded in the current multiple and is a component of the Category Drag discount, distinct from the gaming-label issue. The gap between GAAP operating income and adjusted EBITDA is material. When AppLovin reports 85% EBITDA margins, the comparable GAAP operating margin is closer to 72%. The 72% figure is the right one to use for cross-company comparisons. The headline number requires the asterisk.

The number that matters most is not any of these. It is the revenue growth rate on the e-commerce vertical in the next two quarters. If e-commerce advertising on AXON scales the way gaming did, the 59% overall growth rate either holds or accelerates on a larger base. If it stalls out, the business reverts to a gaming-concentrated platform in a flat market and the growth rate compresses toward single digits within two years. Those two paths do not look alike.

The current price is somewhere between them.

The Short Report Had a Point

AppLovin is not a consensus long. It is one of the most actively shorted large-cap technology companies in the US market. The short thesis has two components. One is mostly noise. One deserves serious attention.

The noise: short sellers, including a widely-circulated 2025 report from Muddy Waters Research, alleged that AppLovin’s ROAS metrics overstate actual advertiser returns. The specific claim is that AXON’s attribution model takes credit for conversions that would have happened organically, inflating the apparent return on ad spend and making the platform look better than it performs. This is a persistent criticism across the performance advertising industry and is not specific to AppLovin. Every major ad platform, including Meta and Google, has faced versions of this allegation over the past decade. The sustained growth in advertiser retention rates and multi-year contract data from AppLovin’s largest spending partners are evidence against the most severe version of the claim. Short sellers are not wrong that attribution is imperfect. Based on available evidence, they have not demonstrated that the imperfection is materially larger at AppLovin than industry standard.

The serious concern is the SEC investigation.

AppLovin’s year-end filings disclosed that the company had received requests for information from the SEC related to its advertising attribution methodology and the accuracy of its performance metrics. The company disclosed it is cooperating with those requests. The distinction matters: a voluntary response to information requests is not the same as a formal SEC investigation, which involves compulsory process and a higher threshold of regulatory concern. No formal order of investigation has been publicly disclosed as at May 2026. SEC processes of this type, from initial requests through to a determination, typically run 12 to 24 months. The overhang is unlikely to resolve quickly in either direction.

This matters for a specific reason. AppLovin’s premium multiple, and the BUY rating attached to it, rests on the assumption that 85% segment EBITDA margins reflect real advertiser value delivered. If the SEC finds that the attribution methodology materially misrepresents performance, two things follow. Advertisers reassess spending based on revised performance expectations. The disclosure risk creates a legal liability exposure that is not quantifiable from public filings. If the first happens, growth decelerates and the multiple compresses simultaneously. If both happen, the stock reprices to a level reflecting a business under active regulatory stress.

That has not happened. AppLovin has disclosed that it is cooperating fully. The company has not restated financials. No adverse finding has been issued.

The tail risk is real. It is the correct answer to the question “what would change this call?”

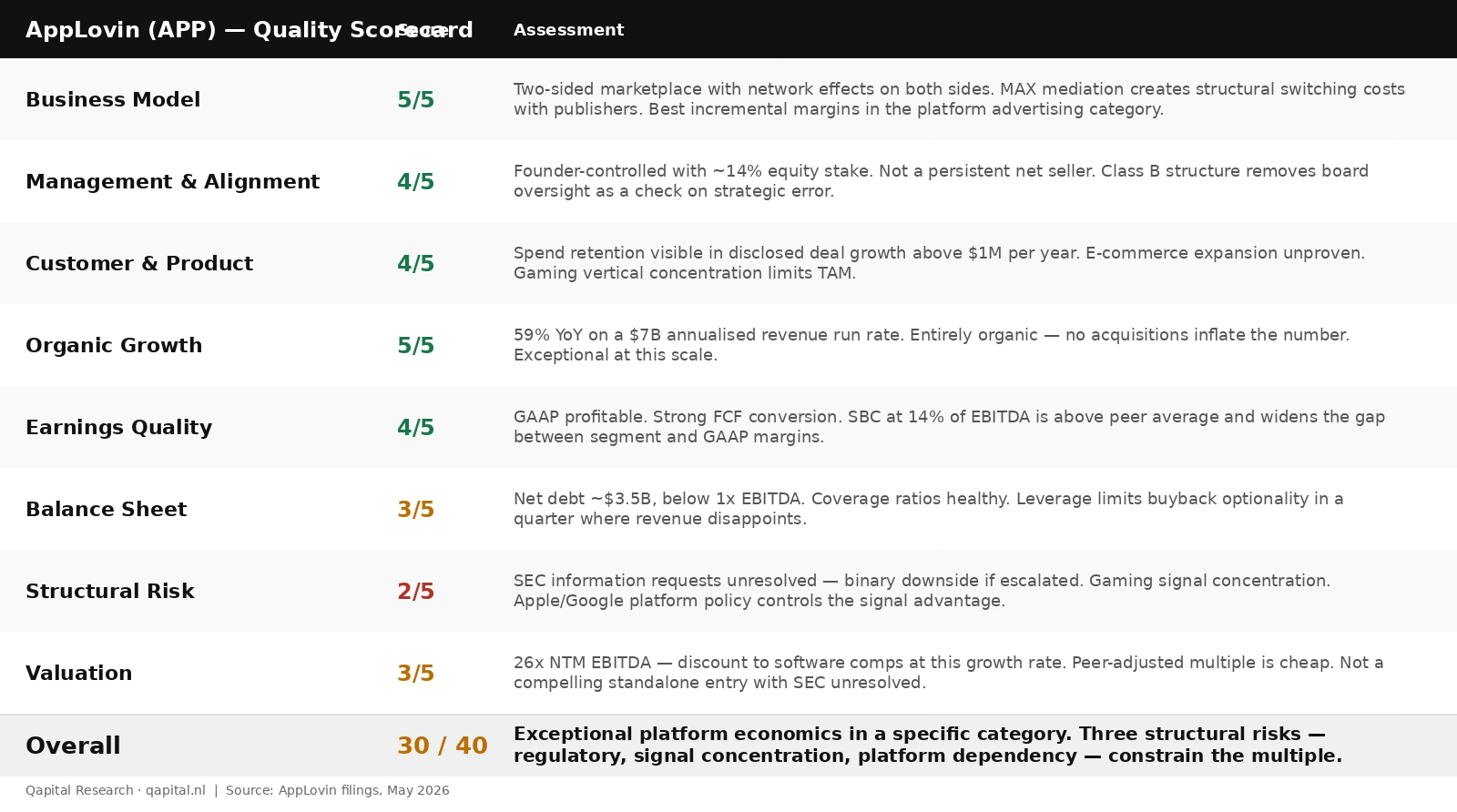

Quality Scorecard

The scorecard reflects a business with exceptional core economics and three structural risks that are not fully resolved at current prices.

Business Model: 5/5. Two-sided marketplace with a proprietary AI recommendation layer. Network effects operate on both the supply and demand side. MAX mediation creates structural stickiness with publishers that is difficult and expensive to remove. 85% segment EBITDA margins on a business growing at 59% are exceptional by any reasonable comparison across ad-tech and most of software, even accounting for the GAAP haircut. The incremental margin structure at scale is one of the strongest in the platform advertising category. This scores at the top of the scale.

Management and Alignment: 4/5. Founder-led, founder-controlled, with significant equity ownership across the executive team. Foroughi has not been a persistent net seller at elevated prices. The governance risk of concentrated voting power is real but substantially mitigated by strong alignment of economic interest. Scores 4 not 5 because the Class B structure removes the board as a meaningful check on strategic error if Foroughi’s thesis proves wrong.

Customer and Product Quality: 4/5. Continued growth in advertiser spending and a disclosed increase in deals above $1 million per year indicate that advertisers are not churning at a meaningful rate. AXON’s performance advantage is reflected in disclosed budget allocation by major gaming advertisers; independent third-party performance benchmarks are not publicly available to verify exact cross-platform deltas. The e-commerce expansion remains unproven. Scores 4 not 5 because the customer base is more concentrated by vertical than the business will eventually require, and the vertical expansion is an open question.

Organic Growth: 5/5. 59% revenue growth is entirely organic. The company sold its games business; all remaining revenue is from the software platform. No acquisitions are inflating the number. 59% growth at a $7 billion annualized revenue run rate is exceptional against any reasonable peer set.

Earnings Quality: 4/5. GAAP profitable with strong FCF conversion. SBC at 14% of EBITDA is above average and requires adjustment before comparing to pure-software peers. FCF is real and growing faster than reported EBITDA. The gap between 85% adjusted EBITDA and 72% GAAP operating margin requires transparency that the company provides but does not highlight in investor communications.

Balance Sheet: 3/5. Net debt of approximately $3.5 billion is manageable at current EBITDA levels. Coverage ratios are healthy and refinancing risk is not near-term. Scores 3 not 4 because the leverage constrains optionality: the company cannot simultaneously retire debt and execute large-scale buybacks in a quarter where revenue disappoints.

Structural Risk: 2/5. Three specific risks score this dimension low. The SEC information requests related to attribution methodology are an unresolved regulatory overhang with a binary downside if they escalate. Dependence on mobile gaming as the primary signal source means a continued flat gaming market limits growth before the e-commerce transition is proven at scale. Apple and Google platform policy controls the environment in which AppLovin’s signal advantage exists; a further restriction on in-app data collection would hit AXON directly. None of the three have a visible resolution timeline.

Valuation: 3/5. 26x next-twelve-months EBITDA is not cheap in absolute terms. It is a discount to where high-margin software platforms with comparable growth rates have historically traded. The Category Drag creates the discount. The question is whether the classification uncertainty resolves. Scores 3 not 4 because the multiple already reflects some of the quality, and the unresolved SEC inquiry means investors buying here are not being compensated for ignoring the tail risk. It is a reasonable entry, not a compelling one on valuation alone.

Overall: 30/40. Exceptional business model in a specific category, with two unresolved structural risks. The score is consistent with a BUY rating at current prices where the mispricing is driven by category confusion rather than a fundamental business problem.

Building a Fair Value

AppLovin’s valuation depends on one question more than any other: what multiple does a reclassified AI advertising platform deserve when the reclassification is only partially complete?

The current multiple, approximately 26x next-twelve-months EBITDA at an enterprise value of around $171 billion, reflects the Category Drag discount applied against a base of real uncertainty. To understand whether that discount is too large, the right comparison is not against gaming companies. It is against platforms with comparable structural characteristics.

Meta Platforms trades at approximately 23x NTM EBITDA with revenue growth around 18%. Alphabet’s advertising business trades at approximately 18x NTM EBITDA growing at 12%. The Trade Desk, the most comparable pure-play programmatic business, trades at approximately 35x NTM EBITDA on growth around 20%. On a growth-adjusted basis, AppLovin at 26x growing at 59% is cheaper than any of those three. Dividing the EV/EBITDA multiple by the growth rate, AppLovin’s ratio is 0.44. Meta’s is 1.28. Alphabet’s is 1.5. The Trade Desk’s is 1.75. The Category Drag discount is real and it is large.

Gaming and ad-tech businesses trade at 15x to 25x. High-margin software platforms with comparable growth trade at 30x to 50x. At 26x, AppLovin sits at the floor of the software range despite having the best growth rate in the category. The market is applying a blend of the two classifications. That is rational given the open risks. It also implies a specific opportunity if those risks resolve.

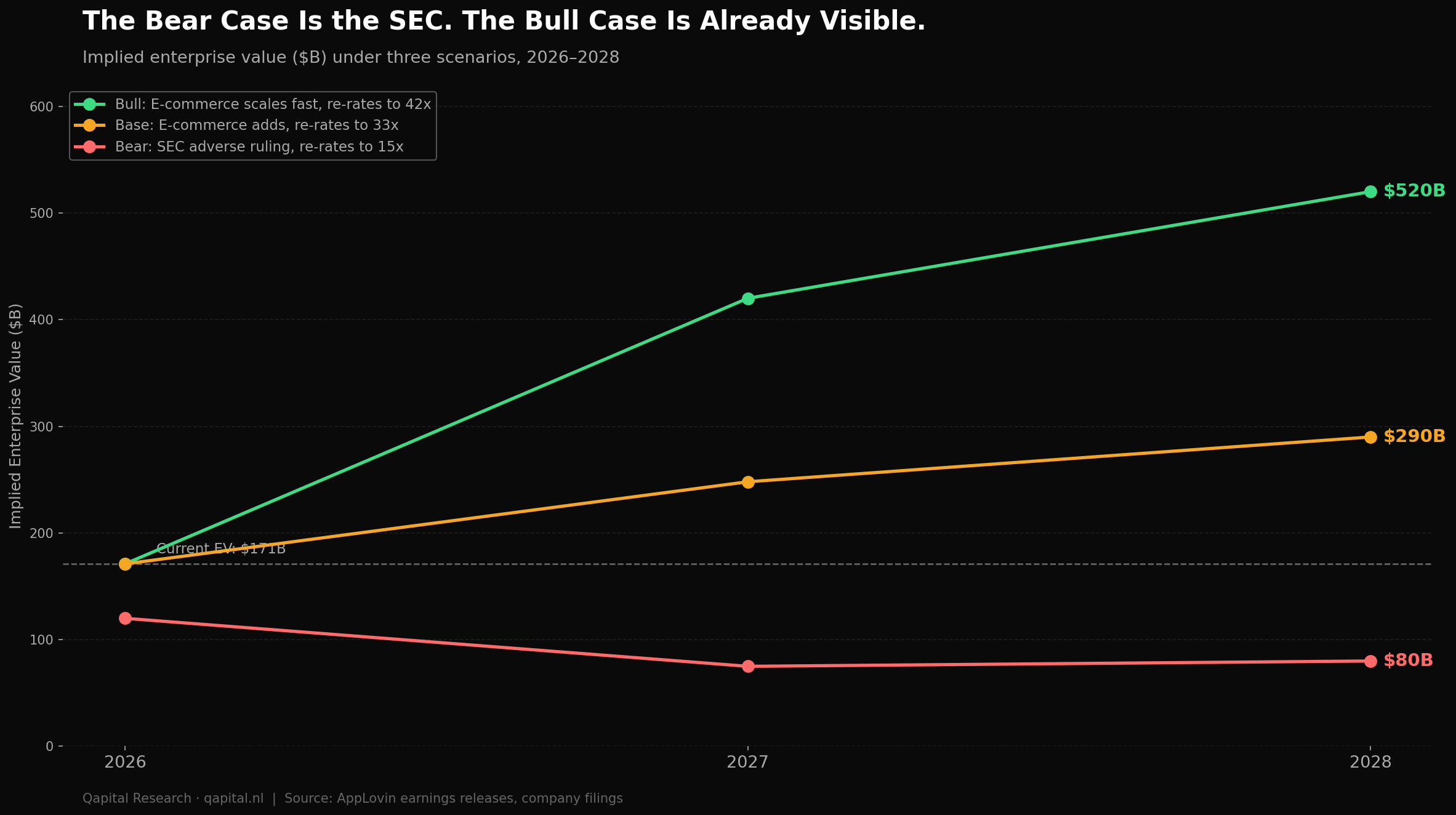

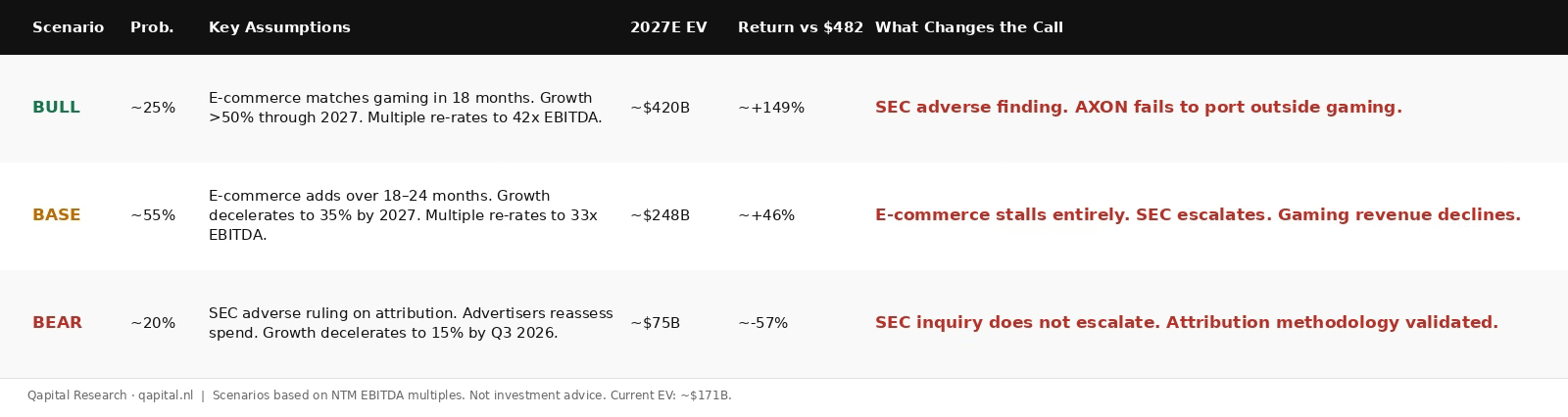

The base case assumes the e-commerce expansion adds material revenue contribution over 18 to 24 months, growth decelerates from 59% toward 35% by 2027 as the mobile gaming base matures, and the SEC inquiry closes without a material adverse finding. EBITDA margins hold in the 80% to 85% range. The business re-rates to 33x on 2027 EBITDA of approximately $7.5 billion. Implied enterprise value: approximately $247 billion by end of 2027. After net debt, implied equity value: approximately $244 billion. That is roughly 46% above the current market capitalization.

The bull case assumes e-commerce scales faster than expected, approaching mobile gaming contribution within 18 months. Revenue growth holds above 50% through 2027. The multiple expands toward 42x on 2027 EBITDA of approximately $10 billion. Implied enterprise value above $420 billion by end of 2027. Implied equity value: approximately $416 billion. Roughly 2.5x the current price.

The bear case assumes the SEC inquiry escalates to a formal investigation and produces an adverse ruling on attribution methodology. Advertisers reassess spending based on revised performance expectations. Growth decelerates to 15% by Q3 2026. The multiple compresses to 15x on an EBITDA base that is now in question. Implied equity value: approximately $72 billion. The current price implies roughly 57% downside in this scenario.

The asymmetry favours the upside in expected-value terms, but it is not extreme. What makes this a BUY rather than a HOLD is probability weighting. The SEC inquiry is informal and early-stage, on a business with no financial restatements and no adverse findings to date. Multi-year advertiser retention data contradicts the most serious version of the short thesis. The base case is more likely than the bear case. The probability-weighted expected value is above the current price, though the margin of safety at $482 is tighter than it was at the $320 lows earlier in the year.

The scenario that does not appear in the three cases above: the e-commerce expansion stalls entirely within two quarters and mobile gaming revenue begins declining rather than growing slowly. That combination compresses the multiple and the earnings simultaneously. It is possible. It is not the most likely outcome given current Q1 advertiser data.

The Bold Call

AppLovin built a real AI recommendation engine, in a real market, producing real cash flow. The software platform reported $1.84 billion in Q1 2026 revenue at 85% EBITDA margins and $1.29 billion in free cash flow in three months. The business grew 59% without acquiring a single company. It has been GAAP profitable for over a year. It converts operating leverage into free cash flow at a rate that most software companies describe in aspirational language rather than quarterly filings.

The steelman for caution is honest and specific. The SEC investigation is not resolved. Attribution methodology is the load-bearing wall of the entire revenue claim: if AXON is taking credit for conversions it did not cause at a material rate, the advertiser relationship reprices and the business model is damaged in ways that take years to fully surface. The mobile gaming market is not growing. E-commerce conversion is promising and unproven on AXON’s infrastructure. The Class B structure means that if Foroughi is wrong about the e-commerce expansion, the correction will come slowly.

For the call to be wrong, one of three things needs to happen: the SEC ruling is adverse and material, the e-commerce expansion delivers nothing after four consecutive quarters of promises, or a hyperscaler builds AXON equivalence using proprietary first-party mobile data at no marginal cost to advertisers.

None of those things have happened.

At approximately 26x next-twelve-months EBITDA for a business growing free cash flow at 59%, the market is pricing Category Drag and regulatory uncertainty, not business failure. The multiple is a discount relative to the correct peer set. The reclassification will not happen on a single quarterly report. It will happen as e-commerce traction becomes undeniable and as the SEC process closes without a finding that damages the revenue model. Both of those things take time. Time at this growth rate is not the enemy.

If the SEC inquiry escalates to a formal investigation with an adverse finding on methodology, this thesis changes immediately. Come back and look again at that point. At $482, the Category Drag discount still compensates for the structural risks, though the margin of safety is materially tighter than it was at the $320 lows earlier in the year. This is not a set-and-forget position. Watch the SEC timeline. Watch the e-commerce contribution numbers in Q2 and Q3 2026.

Our rating: BUY.

The price reflects a gaming company. The business is a platform. That gap closes eventually.

Strip the label. Buy the platform.

This analysis is for informational purposes only and does not constitute investment advice. AppLovin is a listed company (NASDAQ: APP). Financial figures are sourced from AppLovin’s public earnings releases and SEC filings unless otherwise noted. References to the SEC investigation are based on AppLovin’s own disclosures in its year-end filings. E-commerce commentary reflects management guidance from Q1 2026 earnings. Figures relating to short seller reports reference publicly available research attributed to Muddy Waters Research (2025). Analysis reflects conditions as at May 2026.