Constellation Software: Diminishing returns at scale

Ticker: TSX: CSU Current Price: CAD 2,601 (April 21, 2026) All-Time High: CAD 4,800+ (early 2025) Analyst Consensus Target: CAD 4,214 Qapital Rating: CAUTIOUS

The machine that built a legend

If you follow quality investing, you have encountered this story. Mark Leonard, a former venture capitalist, started acquiring small vertical market software companies in 1995. He never sold them. He compounded the free cash flow into the next acquisition. He codified the entire model in annual shareholder letters that became required reading in business schools. He installed radical decentralisation across six operating groups, each running its own acquisition pipeline. Over thirty years, he completed more than 700 acquisitions. The stock compounded at roughly 29% annually from 1995 to 2024.

The legend is real. Leonard built something exceptional.

Between an exceptional business and an exceptional investment sits a question. That question is whether the conditions that produced 29% annual compounding still exist. This article argues they do not, not in the same form, and that the market has only partially priced the transition.

The four signals the market is treating as one

On September 22, 2025, Mark Leonard hosted a 90-minute public webcast on artificial intelligence. He opened with a specific historical reference: Geoffrey Hinton predicted in 2016 that AI would make radiologists obsolete within five years. US radiologist headcount grew from 26,000 to 30,000 in the years that followed. Leonard’s point was precise. AI expands software budgets; it does not contract them.

Three days later, Leonard resigned as President, citing health reasons.

Constellation’s stock had traded above CAD 4,800 in early 2025. It closed at CAD 2,601 on April 21, 2026. That is a 46% decline in fourteen months from a business with $1.7 billion in annual free cash flow available to shareholders, 75% recurring revenue, and 600 portfolio companies embedded in everything from cemetery management software to hospital scheduling systems.

The consensus explanation runs through three separate narratives: AI disruption risk to vertical market software, a leadership vacuum after Leonard’s departure, and general software sector multiple compression. Each is partly true.

They are not three separate problems. They are four simultaneous signals of structural change. Add the PEMS capital deployment pivot to the list. Together they describe a business whose historical compounding conditions are materially less favourable than they were. Not broken. Transitioning. That is a meaningful distinction for how you size the position.

The cognitive trap

The bias driving the mispricing here is narrative permanence: the tendency to treat a model as immortal because it worked for two decades.

Kahneman documented the mechanism. People assess the probability of future outcomes based on how closely they resemble the past, not based on whether the underlying conditions that produced the past still hold. Constellation compounded at roughly 29% annually for thirty years. That number is embedded in the institutional memory of every quality-focused investor. It was produced by specific conditions: thousands of undervalued VMS companies available at 10 to 15 times EBITDA, almost no competition for those targets, a founder who had developed a proprietary acquisition playbook nobody else had codified, and a recurring revenue base so sticky that organic deterioration was invisible against the acquisition growth rate.

Every one of those conditions is now weaker than it was five years ago.

Narrative permanence explains the mispricing on both sides. Bulls hold through a 46% drawdown because the 20-year track record makes every dip feel like an opportunity. That pattern was correct seventeen times before this one. Bears have overcorrected into AI panic, pricing in fundamental model destruction when the evidence supports model deceleration.

The contrarian position is not bullish or bearish on the business. It is bullish on the cash flow base and bearish on the historical multiple. Those two views are compatible. The market is not holding them simultaneously.

The succession

Mark Leonard co-founded Constellation in 1995 with a single acquisition: Trapeze Group, a transit scheduling software company in Hamilton, Ontario. The co-founder of Trapeze was Mark Miller. Thirty years later, Miller runs Constellation.

The succession is more orderly than the initial market reaction suggested. Miller has spent his entire professional career inside the CSI ecosystem: building Trapeze, running Volaris, then serving as COO before his appointment as President in September 2025. He was appointed to the Board of Directors in December 2025. He is an operator by background, not a capital theorist. That distinction matters. The decentralised model means capital allocation was never concentrated in one person alone. Leonard built the playbook in extraordinary detail across thirty years of shareholder letters. The question is whether Miller enforces it with the same discipline.

In March 2026, Leonard announced he would not stand for re-election to the Board at the May 2026 AGM. His statement described a shift to an advisory role with particular focus on the PEMS strategy. He is not fully gone. He is repositioning.

Leonard conducted ten sell transactions over the past five years and zero buys, per the GuruFocus insider record. His most recent disclosed sale was 2,000 shares on March 27, 2025, reducing holdings to 185,090 shares. A founder with strong conviction in a materially undervalued stock tends not to sell into a 40% decline and exit the board. That observation is not a conclusion. It is a data point.

On post-acquisition culture: the official narrative emphasises radical decentralisation and autonomy for acquired companies. Glassdoor reviews from employees at CSI portfolio companies suggest a more mixed picture. Recurring themes include benefit standardisation and a gap between the pre-acquisition pitch and the post-acquisition operational reality. The Harris operating group was named a Glassdoor Best Place to Work in 2020, which cuts the other way. CSI discloses that it monitors annual employee turnover and treats anything above roughly 12% as a concern. Meaningful post-acquisition attrition is an expected and monitored cost in the model, not an exception.

The acquisition engine

Constellation Software’s business model is simple in structure and nearly impossible to replicate at scale: acquire vertical market software companies at prices reflecting their obscurity rather than their quality, never sell them, and compound the free cash flow into the next acquisition.

VMS companies have three structural advantages that make them worth acquiring. Their software is embedded in customer workflows at a level that makes switching technically complex, organisationally disruptive, and often career-threatening for whoever authorises the migration. Their customers are typically small businesses or public sector organisations with limited negotiating power and zero appetite for migration risk. Their markets are so narrow, cemetery management, marina billing, livestock auction platforms, small municipality permitting, that they attract no well-capitalised organic competitors. Pricing power compounds quietly for decades.

The result, across 700-plus acquisitions over thirty years, is a business generating $11.6 billion in annual revenue. $8.7 billion of that, 75%, is maintenance and other recurring fees. Free Cash Flow Available to Shareholders (FCFA2S), CSI’s own preferred metric which excludes non-controlling interest cash flows and is the basis for analyst ROIC calculations, reached $1.683 billion in 2025. The gap between FCFA2S and operating cash flow reflects non-cash amortisation of acquired intangibles, the IRGA liability revaluation discussed in Section 7, and cash flows attributable to minority partners in Topicus and Lumine.

The six operating groups, Volaris (field service and public transit), Harris (public sector, healthcare, utilities), Topicus (European VMS, separately listed on the TSX Venture Exchange), Jonas (hospitality, construction, club management), Perseus (niche verticals including cemetery and funeral software), and Vela (marine and motorsports software), each run their own acquisition pipelines with substantial autonomy on integration decisions. The machine does not require Leonard to function. It requires the discipline he installed to survive him.

The pivot they have not quite explained

The Q4 2025 earnings call introduced a strategic shift that deserves more attention than it received.

CSI announced PEMS: Permanent Engaged Minority Shareholder. Rather than acquiring businesses outright, CSI takes minority stakes in large public companies and engages on governance and capital allocation without paying a control premium. The first meaningful PEMS investment is in Sabre Corporation, the airline reservations and travel technology company. The second expression is Topicus’s acquisition of a 14.84% treasury share stake in Asseco Poland, a publicly listed Eastern European VMS conglomerate with revenues exceeding EUR 3 billion, bringing total CSI group exposure to 24.84% and triggering equity accounting at the Topicus level.

Mark Miller stated in the Q4 2025 call that PEMS “is not driven by AI” and that the acquisition focus has not changed. Both statements may be true.

The economic logic of PEMS is nonetheless difficult to separate from a deployment constraint. CSI generates $1.7 billion in FCFA2S annually and must deploy it at returns above the cost of capital. At the deal sizes that historically produce 25 to 30% ROIC, founder-owned businesses below $20 million in revenue with no auction process, that level of capital deployment requires a very large and consistent pipeline. PEMS is the most plausible response to a pipeline that cannot grow as fast as the capital base. Management has not said this. The capital allocation data, examined over time, will confirm or deny it.

Who is competing for the same targets

Five years ago, Constellation competed against local private equity and regional strategic buyers for VMS targets. That landscape has changed materially.

Roper Technologies deployed $3.3 billion on acquisitions in 2025, including CentralReach ($1.65 billion, autism and IDD care software) and Subsplash ($800 million, faith-based software). Roper has $5 billion available for future M&A and is pursuing the same underlying thesis: recurring-revenue, mission-critical, narrow-market software with pricing power and low churn. Thoma Bravo and Vista Equity Partners actively bid in auctions for mid-market VMS assets. Enghouse Systems, CSI’s closest Canadian analogue, has completed 41 acquisitions averaging $19.8 million each and holds $263 million in cash with zero external debt. Topicus, spun off by CSI in 2021, now competes with the parent for European targets and deployed approximately EUR 700 million in 2025 alone.

A former CSI M&A director quoted on In Practise, a secondary source, stated that “the next 700 companies Constellation acquires will be materially lower quality than the previous 700.” That is an insider perspective rather than a management disclosure.

Independent analysis of CSI’s disclosed FCFA2S against total acquisition consideration suggests portfolio-level returns have compressed from roughly 23.9% in 2023 to approximately 22% in 2025. CSI does not directly disclose cohort-level ROIC for the most recently acquired businesses. Figures for individual year-cohorts are external estimates based on disclosed aggregate data. The direction of compression is consistent. The exact magnitude for any single cohort should be treated as an approximation.

CSI’s disclosed hurdle rates are tiered by target revenue size: 30% IRR for businesses below $1 million in annual revenue, 25% for those between $1 million and $4 million, 20% for those above $4 million, and 15% for larger deals outside CSI’s traditional VMS wheelhouse. Leonard himself has written candidly about the “magnetism effect” of lower hurdle rates, where relaxing the floor gradually pulls the entire capital allocation culture toward the lower target. CSI has not formally reduced its published thresholds. The competitive environment appears to be doing it implicitly.

Management has indicated the pipeline can support approximately 100 new business acquisitions per year before quality deteriorates. Deploying $1.2 to $1.5 billion annually at average deal sizes of $10 to $15 million requires closer to 100 to 150 acquisitions per year. The tension between capital requirements and pipeline quality is structural. PEMS is the most visible attempt to resolve it.

What the numbers actually show

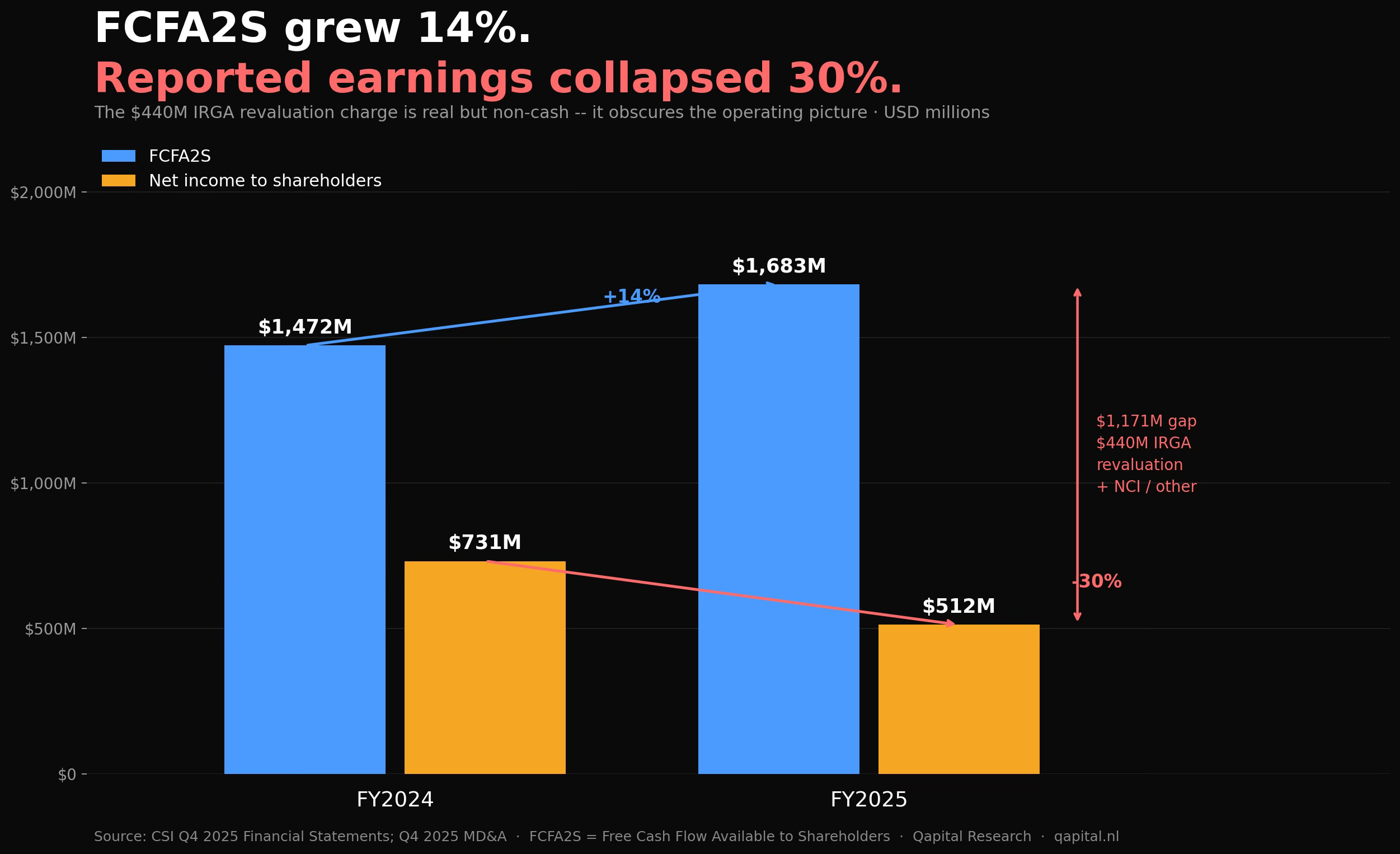

Revenue grew from $8.4 billion in 2023 to $10.1 billion in 2024 to $11.6 billion in 2025, a two-year CAGR of 17.6%. Maintenance and other recurring revenue grew 17.6% in 2025 to $8.7 billion. FCFA2S grew 14% from $1.472 billion in 2024 to $1.683 billion in 2025. These are strong absolute results for a business at this scale.

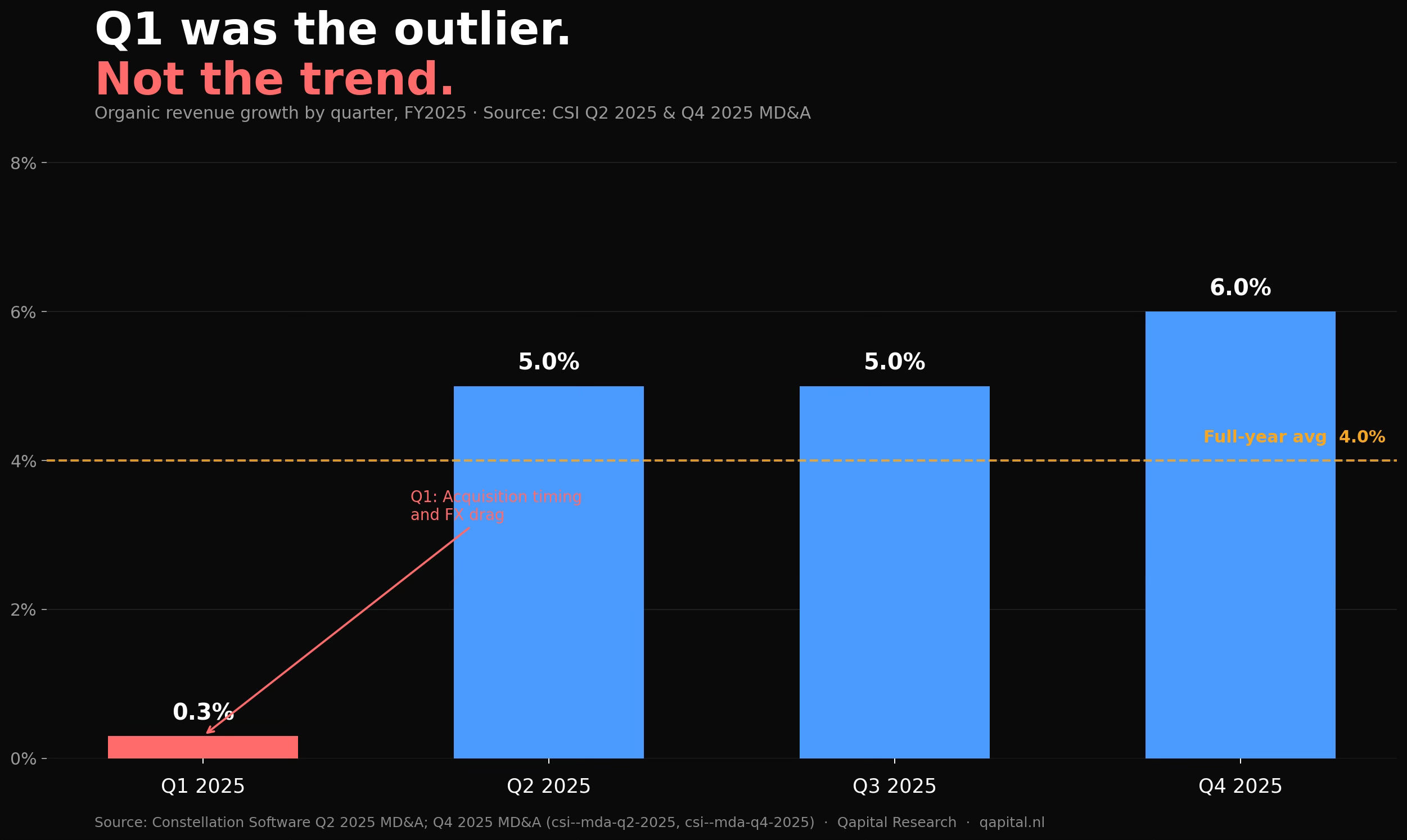

The organic growth profile is where the year becomes more precise. Full-year 2025 organic revenue growth was 4% as reported, or 3% in constant currency. The quarterly distribution matters. Q1 2025 organic growth was 0.3%, a figure disclosed in the Q2 2025 MD&A that received almost no attention in full-year commentary. Q2 and Q3 both recovered to 5%. Q4 2025 came in at 6%, the strongest quarter of the year. The pattern is not linear deterioration. It is a sharp Q1 trough with recovery through the year. For a business deploying $1.2 billion in acquisitions annually, the acquisition-driven growth renders the organic figure nearly invisible in the headline 15.5% total revenue growth. Organic growth is the health indicator for the existing 600-plus portfolio companies. At 3% in constant currency, those businesses are growing roughly in line with inflation. Not losing ground, but not gaining it.

The 2025 net income attributable to common shareholders was $512 million, down from $731 million in 2024, a 30% decline. The primary driver is a $440 million IRGA/TSS membership liability revaluation charge. The Q4 2025 MD&A specifically identifies $252 million of that charge as relating to the Sygnity and Asseco equity investments acquired during the year. The IRGA liability is a financial instrument tied to put and call options held by minority partners in Topicus. Its carrying value is marked to market based on Topicus’s trailing maintenance revenues and net tangible assets. As Topicus performs well, with 2025 revenue of $1.76 billion and operating cash flow of $448 million, the IRGA liability rises in value and produces an accounting loss at the CSI parent. The charge consumed real equity but generated zero cash outflow.

FCFA2S strips out non-cash items including the IRGA revaluation and excludes minority interest cash flows. At $1.683 billion in 2025 (up 14% from $1.472 billion), FCFA2S tells a materially different story than reported net income. The IRGA obligation is real and will eventually settle. Its annual revaluation is driven by Topicus’s performance, which is strong, not by any deterioration in the underlying CSI business.

The Altera situation deserves its own paragraph. Altera Digital Health, the hospital EHR system acquired from Allscripts in 2022 for approximately $725 million and CSI’s largest single acquisition, reported organic revenue declines of 13% year-over-year in constant currency in its most recently disclosed period. Management does not break Altera out separately in the Q4 2025 financial statements. It sits inside the Harris operating group results. A $725 million acquisition declining at 13% organically is the data point on large-deal ROIC that the bulls have not adequately addressed.

Balance sheet: CSI held $3.1 billion in cash at year-end, up from $1.98 billion in 2024. Total recourse debt at the parent level consists of $994 million in senior notes (5.158% due 2029 and 5.461% due 2034) plus $408 million in subordinated debentures. Non-recourse debt at subsidiary level was $2.64 billion. The IRGA liability adds $1.23 billion. At the CSI parent recourse level, net cash is approximately $1.7 billion. The balance sheet is not stressed.

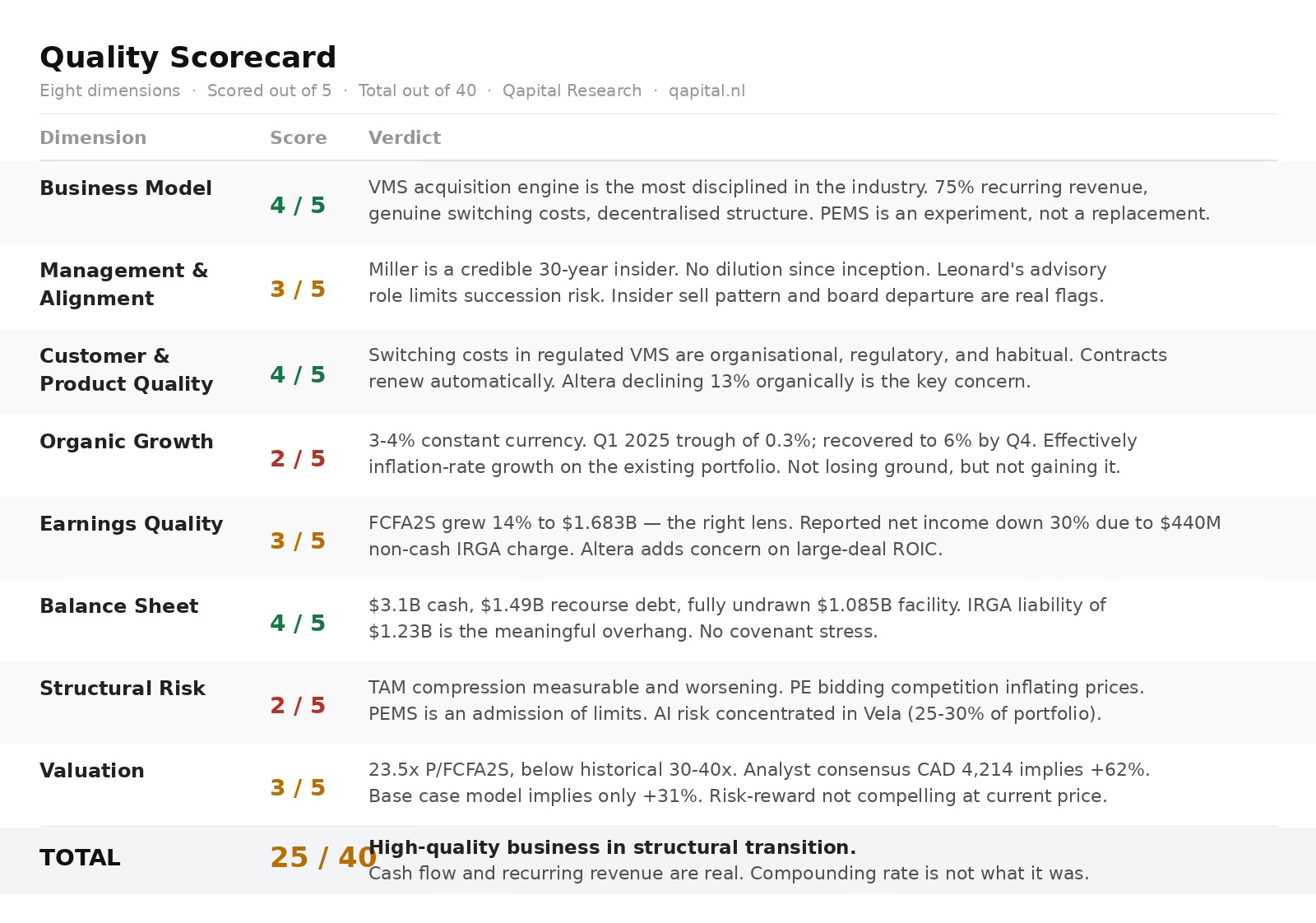

Where the quality holds and where it does not

The quality is real in three places.

The recurring revenue base. $8.7 billion of maintenance and recurring fees, growing at 17.6%, with no meaningful customer concentration and geographic diversity across four regions (USA 42%, UK/Europe 35%, Canada 9%, Other 14%). Switching costs in VMS are not just technical but organisational, regulatory, and habitual. These contracts renew automatically.

The capital allocation infrastructure. The six operating groups each maintain their own acquisition pipelines, underwriting teams, and target relationships. The decentralised model means the machine does not depend on any individual. Leonard built the process. Miller inherits the process. This is structurally different from a company where founder departure would halt acquisition activity.

The AI position. The September 2025 webcast disclosed that 27% of CSI’s business units are developing AI-powered products for customers and that 3% have replaced employees with AI. More significant: the 70% of the portfolio concentrated in regulated industries, healthcare IT, government administration, utilities, public transit, has a moat profile that AI does not easily disrupt on a five-year horizon. Hospital EMR systems, municipal permitting databases, and public transit scheduling platforms carry 30-plus years of accumulated data and regulatory entanglement that AI-native startups cannot replicate. The bear case on AI is real for certain segments. Vela has been identified by external analysts as among the most exposed operating groups. But the overall AI disruption risk, assessed against the 70% of revenue in regulated industries, appears overstated relative to what a 46% stock decline would typically imply.

The quality is uncertain in two places.

Organic growth at 3 to 4% is the thinnest buffer in the model. A business that compounds entirely through acquisitions without organic growth is more fragile than its headline revenue numbers suggest. It requires the acquisition engine to function indefinitely without interruption. Any slowdown in deal flow surfaces immediately in revenue growth.

The PEMS strategy is strategically rational but operationally unproven at scale. The Sabre investment raises a question the earnings call did not answer: what is the expected ROIC framework for a minority stake in a large-cap travel technology company? CSI’s acquisition model generates returns through operational improvements in acquired businesses. A minority investor in a public company with limited board influence cannot execute that playbook. Management states it applies the same IRR discipline to PEMS investments as to acquisitions. The first disclosed return metric on Sabre will tell you more than any management commentary.

The quality scorecard

Total: 25/40. A high-quality business in structural transition. The cash flow is real, the recurring revenue is real, and the AI risk is overstated. The compounding rate the model can deliver going forward is lower than the rate that made the stock famous. By how much is the question that determines everything.

What the price is telling you

CSI trades at approximately CAD 2,601 per share, with 21.19 million shares outstanding and a market capitalisation of approximately CAD 55 billion, roughly USD 39.5 billion at current exchange rates. Against 2025 FCFA2S of USD 1.683 billion, the trailing P/FCFA2S is approximately 23.5x. CSI traded at 30 to 40 times on this measure through most of 2022 to 2024. Analysts covering the stock have characterised the current multiple as among the lowest in over a decade.

The implied FCFA2S growth rate the market is pricing, at a 10% cost of capital and 3% long-run terminal growth rate, is approximately 5 to 7% annually. FCFA2S grew 14% in 2025 and 27% in 2024. That pricing implies meaningful deceleration. The question is whether 5 to 7% is the right expectation for a machine operating at declining marginal returns, without its founder, in a more competitive acquisition environment.

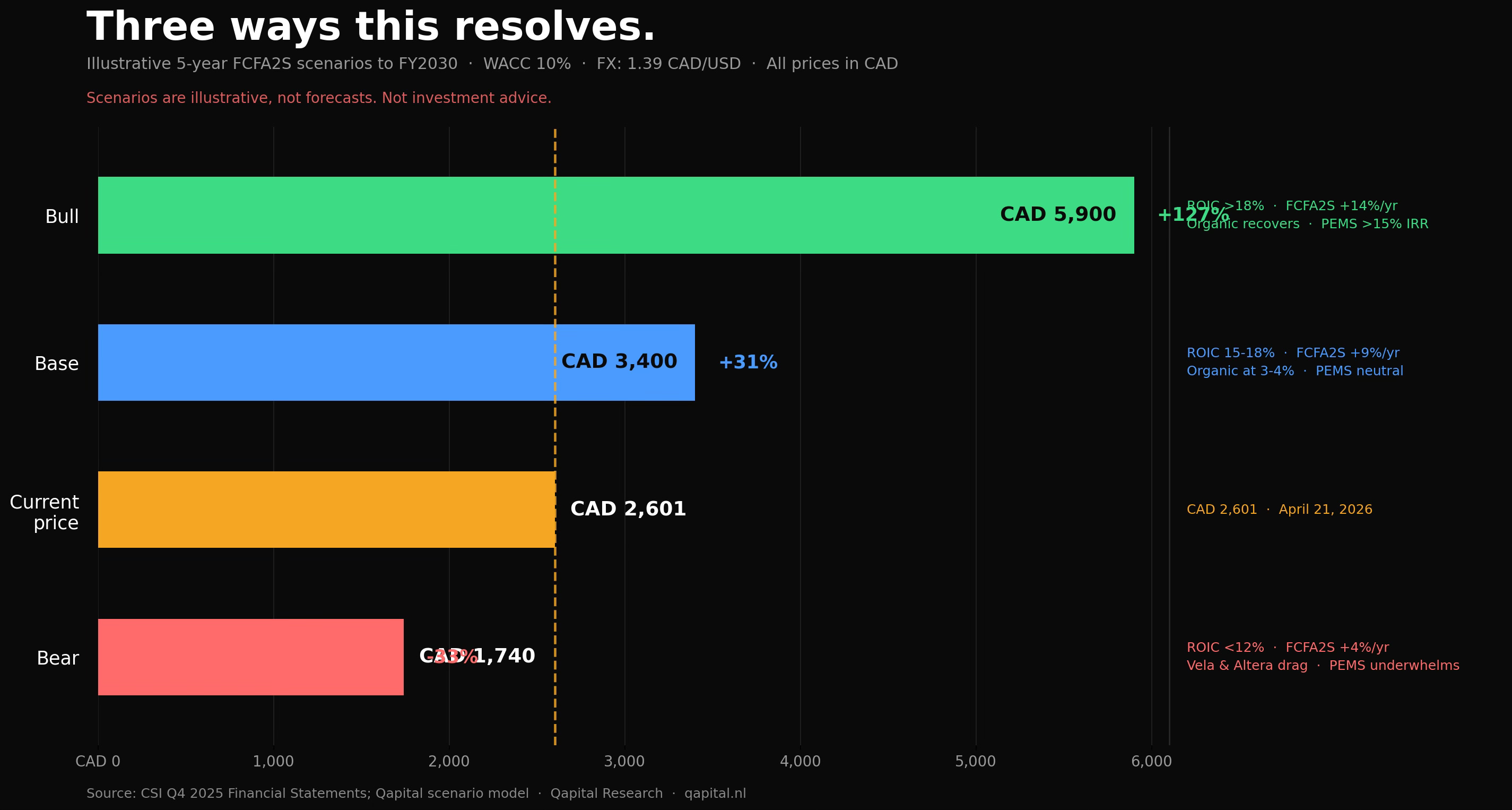

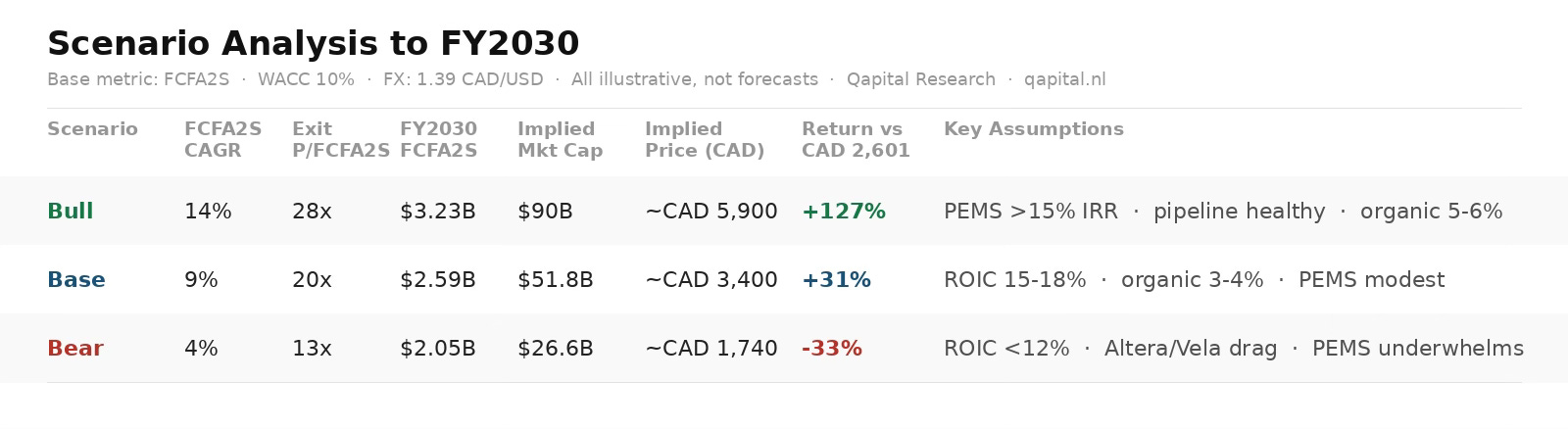

The three-scenario model below runs five years to FY2030. All figures are illustrative. Base metric: FCFA2S. WACC: 10%. FX rate assumed: 1.39 CAD/USD constant throughout.

Key assumptions:

Bull: PEMS proves out above 15% IRR, acquisition pipeline stays healthy, organic growth recovers to 5 to 6%

Base: Acquisition ROIC compresses to 15 to 18%, organic holds at 3 to 4%, PEMS produces modest positive returns

Bear: ROIC on new acquisitions falls below 12%, Altera and Vela drag organic growth toward zero, PEMS underwhelms

The bear case does not destroy capital. The existing FCF base is large enough that catastrophic downside is unlikely without a genuine credit event, which the balance sheet does not support. The bear case risk is years of flat real returns, not permanent loss. That is a meaningful distinction for how you size the position.

The base case, at roughly 55% probability, assumes FCFA2S compounds at 9% annually through FY2030 and CSI sustains a 20x P/FCFA2S exit multiple as a recognised quality compounder at lower growth expectations. The business performs. The multiple does not recover to 35 to 40x. Investors who entered at those levels take a multi-year pause before real returns accrue.

The bold call

Mark Leonard built something exceptional. The decentralised structure, the thirty years of compounding, the playbook that survived its author: all of it is real.

But the investor community following CSI has attached a permanent-compounder premium to a business whose marginal returns are measurably declining. FCFA2S portfolio-level returns have compressed from roughly 24% in 2023 to approximately 22% in 2025. The acquisition pipeline faces PE bidding competition that did not exist a decade ago. Organic growth sits at 3 to 4%, effectively inflation. The founder has left. The company is now making minority investments in large public companies, a fundamentally different activity from what built its track record. The stock is 46% below its all-time high.

The most important number to watch is not Q2 2026 revenue. It is the first disclosed return metric on the Sabre PEMS investment, expected in the next substantial shareholder letter. If PEMS produces a return above 12%, the bull case probability increases substantially. If Sabre deteriorates or the stake is written down, the bear case accelerates.

The second number is H1 2026 organic growth. Q1 2025 came in at 0.3%. It recovered to 5 to 6% for the rest of the year. If that pattern holds into 2026, the base case is on track. If H1 2026 reverts below 2%, with Altera declining and Vela facing AI-native competition, the bear case becomes the modal scenario.

Our rating: CAUTIOUS. The business deserves respect. The narrative of the unstoppable compounder does not survive contact with the current numbers. CSI at CAD 1,740, if organic growth stabilises, Altera recovers, and PEMS finds a return framework, becomes an interesting conversation. At CAD 2,601, with ROIC compressing, organic growth at inflation, the founder departed, and PEMS unproven, the risk-reward is not compelling.

The paid platforms told you this was a permanent 29% compounder. The FCFA2S cohort data says otherwise.

Trust the cash flow.

Primary sources: Constellation Software Inc. Q4/FY 2025 Financial Statements; Q4 2025 Press Release (csi---press-release-q4-2025---final.pdf, csisoftware.com); Q4 2025 Shareholder Report (q4-2025-shareholder-report.pdf, csisoftware.com); Q4 2025 MD&A (csi---mda-q4-2025---final.pdf, csisoftware.com); Q2 2025 MD&A (csi---mda-q2-2025---final.pdf, csisoftware.com, source for Q1 2025 organic growth rate). Secondary sources: CSI AI Strategy Webcast transcript (September 22, 2025, via GuruFocus); GlobeNewswire, Mark Leonard Presidential Resignation (September 25, 2025); GlobeNewswire, Mark Leonard Board Departure (March 27, 2026); Western Investor, Mark Miller Appointment; CSI Board Appointment press release (December 2025, csisoftware.com); In Practise, Constellation Software: Competition, Hurdle Rates and Deal Flow; Seeking Alpha, Deteriorating ROIC and High Valuation, Fading Excellence; The Compounding Tortoise, Q4 and FY 2025 Constellation Software Full Recap; LongYield, Constellation Software and the AI Reckoning; FTRInvestors, Constellation Software vs. Roper Technologies; Kavout, PEMS Strategy Analysis; Roper Technologies 2025 Annual Earnings Release (ropertech.com); Enghouse Systems acquisition history (Tracxn); GuruFocus, Mark Leonard insider trading record.

Disclosure: No current position in Constellation Software Inc. at time of publication.