Palantir: The best quarter that nobody believed

Ticker: NASDAQ: PLTR Current Price: Around $134 (as at May 7, 2026) All-Time High: $207.52 (November 2025) Analyst Consensus Target: $194.77 (Buy consensus, wide dispersion) Notable Short: Michael Burry, ~$1B notional position, stated fair value below $50

The day the numbers weren’t enough

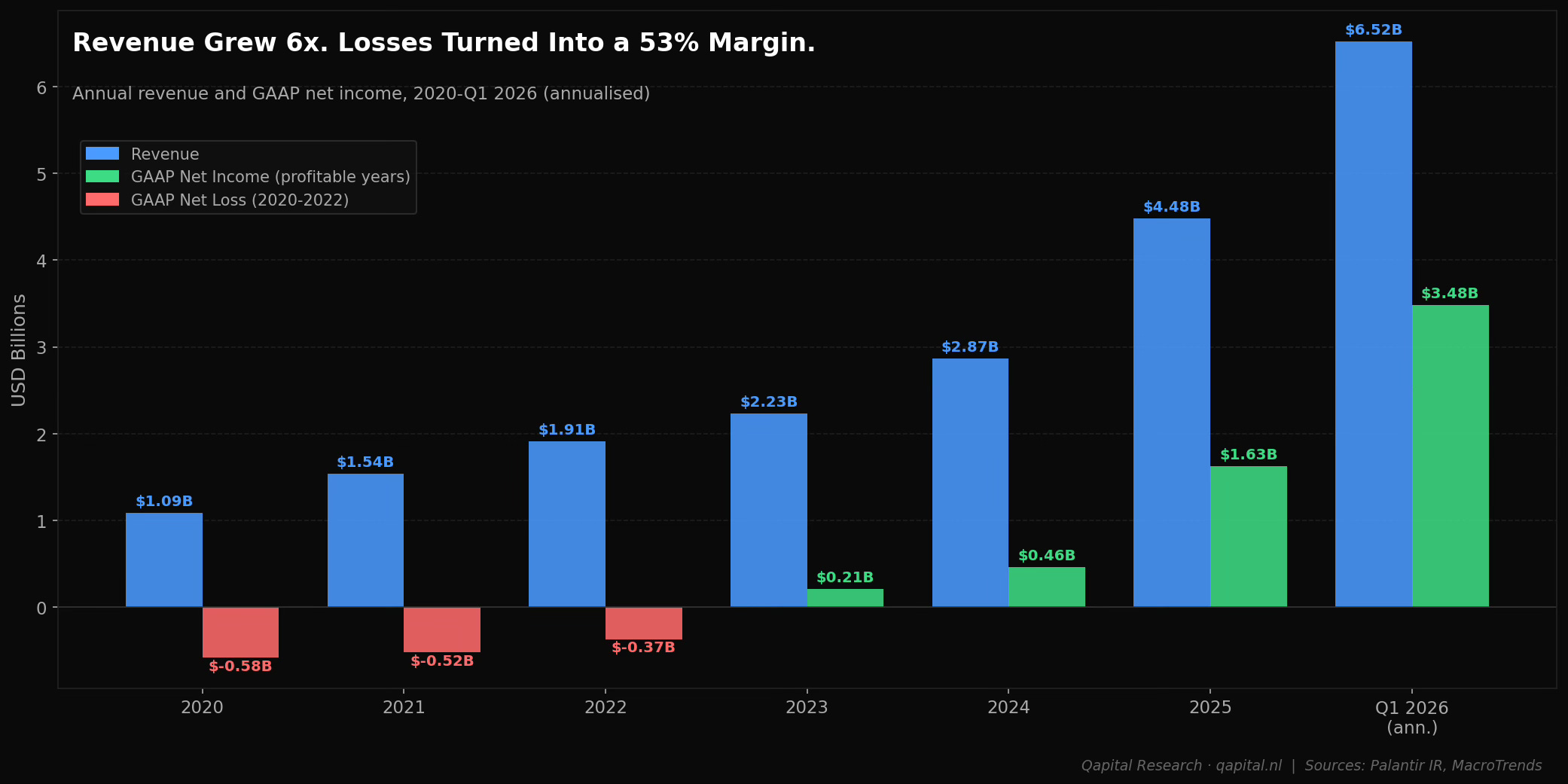

On May 5, 2026, Palantir Technologies reported the best quarter in its history by every metric that matters. Revenue grew 85% year-over-year to $1.63 billion, the fastest pace since the company went public in 2020. US commercial revenue more than doubled. GAAP net income hit $871 million, a 53% profit margin on the most complex enterprise software business in the world. Free cash flow was $925 million. The company raised its full-year revenue guidance to $7.65 billion, implying 71% growth, and crushed every analyst estimate on the board.

The stock fell.

It has fallen roughly 30% from its all-time high, set around $207 in November 2025. Year to date in 2026, Palantir is down approximately 23%, making it one of the worst-performing large-cap technology stocks in a market that has been broadly cautious. The Seoul Economic Daily’s headline captured it precisely: “Record Revenue Fails to Impress Market.”

This is the starting point for everything that follows. When a company posts its best quarter ever and the market responds by selling it, one of two things is true. Either the market is wrong and this is one of the great buying opportunities in modern technology investing. Or the market is telling you something that the quarter does not.

We think the market is telling you something.

The exception reflex

Here is how the bull case for Palantir is typically made.

The company is building the operating system for AI-era enterprises and governments. Alex Karp has been saying this for years, and the data is now proving him right. No other software company on earth is growing revenue at 85% at $6.5 billion annualised run rate. No other company has a Rule of 40 score of 145%, a metric that combines revenue growth and profit margin and was previously considered impossible above 100%. No other company has positioned itself at the intersection of government intelligence, enterprise data, and AI deployment with the same depth of customer relationships.

When you raise the question of valuation, 42 times next year’s revenue, the response from the bull community is swift and specific. You are applying an old framework to a new category. This is not a software company in the traditional sense. It is infrastructure for Western civilization, in Karp’s own framing. Comparing its multiple to Salesforce or ServiceNow is a category error. The right comparisons are Amazon Web Services or Microsoft Azure in their early phases, when no multiple seemed too high for what they were becoming.

This reasoning pattern has a name. Call it the exception reflex: the cognitive tendency of investors in truly exceptional businesses to treat valuation skepticism as a failure of imagination rather than a legitimate constraint. It is not unique to Palantir. It has appeared at every major technology inflection point. The exception reflex does not mean the business is bad. It means the question of what you pay for it has been moved off the table. Moving a question off the table is never a good sign for investment returns.

The exception reflex is particularly powerful when the founding CEO is a philosopher. Karp has a doctorate in social theory from Goethe University Frankfurt. He speaks in frameworks where software companies are instruments of civilizational survival. He published a book, “The Technological Republic,” positioning Palantir not as a software vendor but as a moral actor in the struggle to preserve Western democratic values. Time magazine named him one of the world’s 100 most influential people in 2025. He is, objectively, one of the most compelling communicators in technology, and his framing has influenced not just investor perception but how Palantir’s own employees think about their work.

The result is a company where the investment thesis has become almost entirely narrative rather than quantitative. Not because the numbers are bad. The numbers are extraordinary. But because the narrative has grown large enough to make the numbers feel beside the point.

They are not beside the point.

The Philosopher-King and his machine

Understanding Palantir requires understanding Alex Karp, because there is no other major technology company where the CEO’s intellectual persona is this deeply embedded in the investment thesis.

Karp co-founded Palantir in 2003 with Peter Thiel, Nathan Gettings, Joe Lonsdale, and Stephen Cohen. The company spent its first decade building surveillance and data fusion tools for US intelligence agencies, initially funded by the CIA through In-Q-Tel. It did not go public until 2020, a 17-year private incubation. The patience required to build this way is rare. Most software companies either race to public markets or sell to a strategic. Palantir built something harder to understand and harder to copy.

Karp owns roughly 2.5% of the company outright, but controls a substantial majority of voting power through a multi-class share structure that concentrates decision-making with the founders. This is absolute founder control. He cannot be removed. He does not answer to a board in the traditional sense. This is a feature for long-term holders who believe in his vision. It is also a risk that has no obvious mitigation.

The compensation structure is unusual. Karp’s total compensation in recent years has run into hundreds of millions of dollars, primarily through stock grants. He has been a net seller of shares periodically, which the bull community notes is common for concentrated founders managing personal liquidity. The sales are disclosed and the ownership stake remains substantial. Unlike some founder-CEOs who talk alignment and then quietly sell, Karp’s position is transparent.

What is harder to evaluate is the relationship between the philosophical framing and the commercial reality. Karp has positioned Palantir as existing to ensure that “democratic governments, and not those who oppose them, wield the most potent capabilities in the AI age.” This framing does two things. It makes the company morally appealing to a specific kind of investor. And it justifies unusual customer selectivity, Palantir has turned away contracts it deems inconsistent with its values, and an unusual public profile for a software company.

It also attracts scrutiny. Palantir’s work with the IRS on large-scale data mining, its contracts with ICE for immigration enforcement data, and its role in various intelligence applications have generated consistent controversy. A 2026 opinion piece called its manifesto “dystopian.” Lawsuits under the Privacy Act of 1974 are ongoing. None of this has damaged the commercial business in a measurable way so far. It is, however, a reputational risk that concentrates in the political domain and could shift quickly with a change in administration.

What AIP actually does

Palantir operates through two main platforms. Foundry is the older product: a data integration and operations platform that connects disparate enterprise data sources, structures them into what Palantir calls an “ontology” (a representation of real-world objects and their relationships), and enables analysis and workflow automation on top. Foundry has been the backbone of the company’s government contracts for years.

AIP, the AI Platform, is the newer product launched in 2023 and now the primary commercial growth driver. AIP takes the ontology layer from Foundry and wires it to large language models and AI agents, allowing enterprises to build AI-powered workflows on top of their own operational data. The pitch is specific: rather than chatting with a generic AI about general topics, a logistics company can deploy an AI agent that reasons about its actual trucks, routes, inventory, and supplier relationships in real time.

This is a real and durable capability. The ontology layer is not trivial to replicate. It requires deep integration with client systems, significant data engineering, and ongoing configuration. This is also why the AIP Boot Camp model exists: Palantir sends forward-deployed engineers directly into customer operations for five-day intensive sessions, building working prototypes on actual client data. The customer goes from zero to a functioning AI workflow in one week.

The bull community correctly identifies this as Palantir’s core moat. Once your operational data is structured into Palantir’s ontology and your AI workflows are running on AIP, switching costs are significant. The data model, the workflows, and the AI agents are all built on Palantir’s stack. Ripping it out is a major undertaking. This is sticky software at the operations layer, where switching costs are highest.

The bear community, including Jefferies analyst Brent Thill, raises the legitimate counterpoint: forward-deployed engineers are not a scalable delivery model. A traditional SaaS company grows revenue without proportionally growing headcount. Palantir’s model requires smart, senior engineers embedded at each client. As the customer base grows, so does the required engineering labor. The company has been working to automate and systematise the Boot Camp model, but the fundamental question of whether AIP can scale like Salesforce or whether it will always require consulting-level deployment effort is unanswered by the data so far.

The average contract value at Palantir is approximately $4 million annually, four times the typical enterprise SaaS deal. This is consistent with a model that involves significant deployment effort and is priced accordingly. In Q1 2026, Palantir closed 206 deals worth at least $1 million each and 47 deals worth at least $10 million. Total contract value booked in a single quarter was $2.41 billion, up 61% year-over-year. The pipeline is real and growing.

But pipeline growth and deployment scalability are two different questions. Q1 2026 proves the pipeline is there. It does not yet prove that Palantir can serve 10,000 enterprise customers with the same depth it currently brings to 1,000.

The competition problem nobody talks about

The standard competitive framing around Palantir positions it against other data and AI platforms: Snowflake, Databricks, C3.ai, or the analytical tools within major cloud providers. This framing is partially accurate but misses the more important structural question.

The real competition for Palantir is not another dedicated AI platform. It is the native AI capabilities being embedded into Microsoft Azure, Amazon Web Services, and Google Cloud Platform, the services that already host most of the enterprise data that Palantir wants to reason about.

Microsoft has Copilot integrated across its entire enterprise suite, with direct access to Teams, SharePoint, Dynamics, and Azure data stores. AWS has Bedrock and SageMaker. Google has Vertex AI. Each of these hyperscalers has a fundamental advantage Palantir does not: they already own the pipes through which enterprise data flows. If Microsoft can offer an AI operations layer that runs on the data already living in Azure, most enterprises will ask whether they need a separate Palantir deployment at all.

Palantir’s answer is that its ontology is deeper, its AI agents are more capable in complex operational environments, and its government-grade security posture is unmatched. All of this is true in the specific domains where Palantir excels, primarily complex multi-agency government operations and industrial enterprises with messy, multi-source data. It is less clearly true in the broader mid-market where AIP is now trying to grow.

International commercial revenue in Q1 2026 grew only 26% year-over-year, compared to 133% in the US commercial segment. This is not a minor gap. It suggests that outside Palantir’s home market, where brand recognition, government relationships, and cultural alignment with Karp’s positioning are strongest, the product has not found the same traction. The hyperscaler competition is global. Palantir’s advantage, for now, is predominantly American.

In Q1 2026, international commercial revenue was $179 million. US commercial revenue was $595 million. The US is not just growing faster; it is three times larger. For a company guiding to 71% full-year growth, sustaining that number requires international commercial to accelerate materially. The Q1 data does not show that happening.

Four numbers that matter

Palantir’s financial history before 2023 is a story of losses. The company burned cash for over a decade, funding its government intelligence work and commercial platform development before turning GAAP profitable. Annual net losses ran from $580 million in 2020 to $371 million in 2022. The first year of full GAAP profitability was 2023, at $210 million.

What happened next is remarkable. GAAP net income went from $210 million in 2023 to $462 million in 2024 to $1.625 billion in 2025, a 600% increase in three years. In Q1 2026 alone, the company generated $871 million in GAAP net income at a 53% margin.

Four numbers clarify what is happening and what is at stake.

Number one: 42. This is the approximate EV/Revenue multiple on Palantir’s full-year 2026 guidance of $7.65 billion, using an enterprise value of roughly $325 billion at current prices. For context, Snowflake at peak AI excitement in 2021 traded at 80 times revenue but was much smaller and growing from a lower base. Microsoft, the most valuable software company in the world, trades at around 14 times revenue. At 42 times forward revenue, Palantir is priced as if it is about to become, in relative terms, significantly more dominant than Microsoft. That is possible. It requires believing many things simultaneously.

Number two: 107. At current prices, Palantir trades at approximately 107 times its full-year 2025 GAAP earnings. The S&P 500 as a whole trades at roughly 21 times earnings. The premium Palantir commands over the index is not 50% or 100%. It is roughly 400%. Even if you annualise Q1 2026’s extraordinary $871 million GAAP net income, implying roughly $3.5 billion for the full year, the forward PE is still around 94 times. At the world’s highest growth rate, this is the cost of admission.

Number three: $808 million. This is the rough annualised run rate of Palantir’s stock-based compensation, based on Q1 2026’s $202 million quarterly figure. Unlike the KPG situation where NPATA strips out an expense that represents real acquisition economics, Palantir’s SBC adjustment is more conventional. The GAAP story is improving regardless: $202 million of SBC in a quarter where GAAP net income was $871 million means the SBC, while real and dilutive, is now a smaller fraction of an increasingly large profit base. SBC as a percentage of revenue was approximately 12% in Q1 2026, down from 15% in 2025 and significantly higher levels in earlier years. The trend is right. The absolute number is still large.

Number four: 26. This is the year-over-year growth rate of Palantir’s international commercial revenue in Q1 2026. Everything else about the company is growing at 85-133%. International commercial is growing at 26%. When most of your growth is concentrated in one market and one segment, and your valuation prices in global enterprise dominance, the gap between those two facts is where the investment risk lives.

The DOGE paradox and the Two-Speed business

The most structurally interesting contradiction in the Palantir investment case is almost never discussed directly by the bull community.

Alex Karp and Palantir have been among the most prominent Silicon Valley voices supporting the Trump administration’s government efficiency agenda. Karp appeared publicly alongside administration officials. Palantir positioned itself as the technology partner for federal modernisation, for streamlining agencies, cutting redundancies, and deploying AI to make government work better with fewer resources.

In Q1 2026, 42% of Palantir’s total revenue, $687 million of $1.63 billion, came from US government contracts. The company has contracts spanning the Army, IRS, ICE, Space Force, and Treasury Department. It has publicly disclosed over $900 million in new federal contract wins.

The DOGE paradox is this: you cannot simultaneously advocate for cutting government spending and depend on government spending for nearly half your revenue without accepting a structural tension that the market will eventually price. If DOGE succeeds in its stated mission, some of the agencies that are currently writing Palantir the largest checks will have smaller budgets. Palantir’s stated answer, that it will be the consolidation play as agencies reduce headcount and replace people with AI, is coherent and may prove correct. It is also untested at scale.

Keep reading with a 7-day free trial

Subscribe to Qapital to keep reading this post and get 7 days of free access to the full post archives.