Rocket Lab: Great Business, Dangerous Price

Ticker: NASDAQ: RKLB

Price (June 2026): ~$118, already ~22% below the all-time high of ~$151 set May 27, 2026

Market Cap: ~$66 billion

TTM Revenue: ~$680 million (~46% growth)

Implied Valuation: ~95x trailing sales, still pre-profit

The Number That Doesn’t Fit the Name

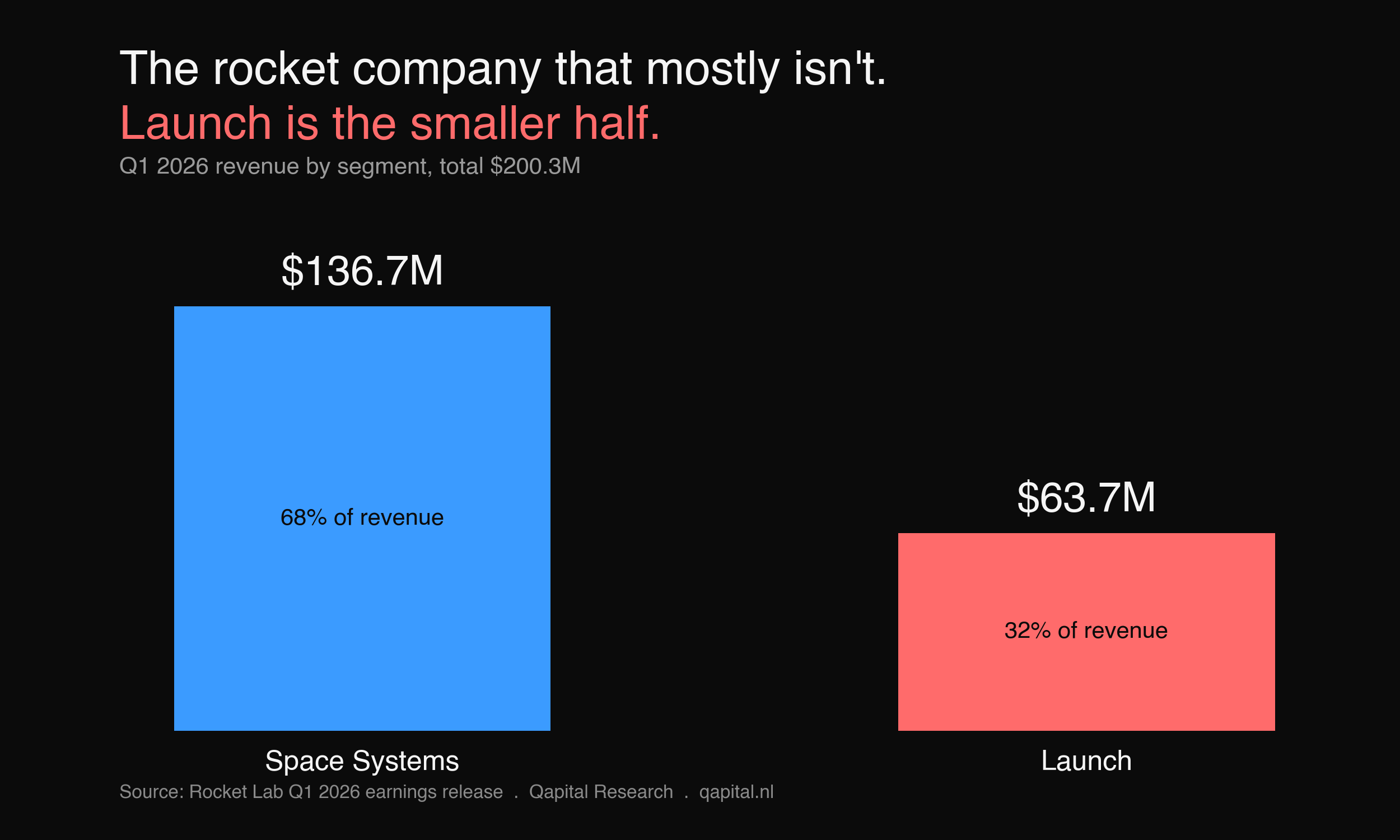

In the first quarter of 2026, Rocket Lab reported $200.3 million in revenue, its first quarter above $200 million and a 63.5% jump on the prior year. The headline is impressive. The split is the story.

Space Systems brought in $136.7 million. Launch brought in $63.7 million.

The company with “Rocket” in its name earns roughly two-thirds of its money notlaunching rockets. It earns it building satellites, selling components, and assembling spacecraft for other people. Launch, the part everyone talks about, is the smaller half, and has been for a while.

That gap between what the company does and what the market thinks it does is the whole article. The market isn’t pricing the business Rocket Lab has. It’s pricing the business it imagines. And the distance between those two has a name in behavioral finance, one we’ll come back to, because it’s also the name of the trap.

The Narrative the Market Is Buying

Ask a retail investor what Rocket Lab is, and the answer is some version of “the next SpaceX.” That sentence does an enormous amount of work, and most of it is wrong.

The framing took hold for an understandable reason. With SpaceX itself private, Rocket Lab has been the only Western, vertically integrated, end-to-end space company that retail investors could actually own. When you can’t buy the leader, you bid up the closest available substitute. That’s a flow, not a thesis. And it isn’t only retail doing it. At a $66 billion market cap, institutions dominate the register, and plenty of them are buying the same proxy logic.

The timing makes it sharper. SpaceX is set to go public this Friday, June 12, at a reported valuation near $1.75 trillion, what would be the largest IPO in history. The attention pouring into the sector ahead of it has lifted every adjacent name, and Rocket Lab printed an all-time high of about $151 on May 27. It has since slipped to about $118, off roughly 22% from that peak in under two weeks, even though the hype that drove it has barely cooled. The stock is still up several-fold in twelve months. And here is the tell: even Stifel’s raised target of $132, lifted partly on momentum the sector is borrowing from the SpaceX event itself, sits only about 12% above today’s ~$118. The analysts who actually build a model for this company are not underwriting the “next SpaceX” dream. The gap between $132 and the prices the market narrative implies is sentiment, not analysis. The point is not that the top is in. No one can know that. The point is narrower: the stock has already given back nearly a quarter of its value while the enthusiasm that drove it remains intact, which is a measure of how much of the price rests on sentiment rather than results.

Here’s the trap, named directly. Investors are anchoring a $66 billion valuation for Rocket Lab to SpaceX’s $1.75 trillion, as if proximity to the leader transfers the leader’s economics. It doesn’t. SpaceX flies the most-used orbital rocket on Earth, runs a profitable global satellite-internet business with millions of subscribers, and generates cash. Rocket Lab flies a small rocket, hasn’t yet flown its medium one, and loses money. The two are in the same industry the way a regional carrier and a flag airline are in the same industry.

The mental model on offer is “buy the space theme before SpaceX lists.” The reality is a specific company, at a specific price, with a specific binary catalyst that has already slipped once. Those are not the same purchase, and telling them apart is the whole job for an investor today.

Peter Beck and the Vertical-Integration Bet

Rocket Lab is founder-led, and the founder is the reason it’s more than a launch story.

Peter Beck started the company in New Zealand and built Electron from nothing into the second-most-used orbital rocket in the United States. Years ago he made a strategic decision that’s now visible in every earnings split: don’t be a launch company, be a space company. The logic is hard to argue with. Launch is the hardest, most capital-intensive, lumpiest link in the value chain, and on its own it’s a brutal business. The durable money sits in what goes on top of the rocket, and in what the satellites do once they’re up there.

So Beck pushed Rocket Lab up the stack: reaction wheels, solar arrays, star trackers, separation systems, flight software, and increasingly whole spacecraft buses. The “Flatellite” platform is the next step: a standardized satellite built for volume, both for customers and, eventually, for Rocket Lab’s own constellations and services.

Beck holds a meaningful equity stake, and his credibility with engineers and customers is a genuine asset in a field where execution is the only thing that matters. The alignment is real. The caveat is dilution: Rocket Lab has repeatedly funded its ambition by issuing stock, and shareholders have paid for the vertical-integration strategy in ownership as well as cash.

How the Two Engines Actually Work

Launch. Electron is a small-lift rocket serving dedicated and rideshare missions for governments and commercial operators. It’s a real franchise: reliable cadence, a record backlog of more than 70 missions, and 31 new Electron and HASTE contracts signed in Q1 2026 alone, more than the company signed in all of 2025. HASTE, the suborbital variant, sells into hypersonic-test demand, a direct beneficiary of rising defense budgets. Launch is strategically central and commercially modest: low-margin, capital-heavy, and existing mostly to anchor the relationships that feed the rest of the company.

Space Systems. This is the larger and structurally better half. Rocket Lab sells the components and subsystems that go inside other companies’ satellites, and it builds complete spacecraft. The margins are higher, the revenue is less lumpy, the backlog is substantial, and the customer list spans NASA, the US Space Force, and commercial constellation operators. As this segment scales, and especially if Flatellite turns Rocket Lab into an operator of its own constellations, the economics start to look less like a rocket maker’s and more like a recurring space-infrastructure business.

That mix shift is the actual quality story. It’s also the one the “next SpaceX” narrative completely ignores.

Neutron: The Catalyst That Decides the Multiple

Everything bullish about the stock price assumes Neutron.

Neutron is Rocket Lab’s medium-lift, partially reusable rocket, designed to carry roughly thirteen tonnes and to compete for the constellation-deployment and national-security launch market that Electron is far too small to touch. If it flies and ramps, Rocket Lab graduates from niche small-launch provider to credible competitor for the contracts that actually move the revenue line. That graduation is the re-rating the bulls are paying for.

It hasn’t flown. And the road has been rough. On January 21, a first-stage propellant tank ruptured during hydrostatic pressure testing. Rocket Lab is redesigning the tank, including a move to automated fiber-placement manufacturing, and the debut has slipped to no earlier than the fourth quarter of 2026, with FAA permits filed for a window running through year-end. The Archimedes engine and the second stage keep clearing milestones, and management is holding the Q4 line. But first launches of new rockets slip as a rule, not an exception.

There is one genuinely encouraging signal. Rocket Lab booked its first five commercial Neutron contracts in Q1, the first time customers have publicly committed to a vehicle that hasn’t left the ground. That’s the market voting with money on a rocket still bolted to the test stand.

Read the catalyst honestly: Neutron is a high-variance event with a long fuse, a genuinely wide range of outcomes on a timeline that keeps slipping, not a clean fifty-fifty. A clean debut re-rates the stock. Another tank failure, or a slip into late 2027, knocks out the one catalyst that justifies paying 95x sales rather than the far lower multiple the business would warrant on Space Systems alone. The point is precise: Space Systems supports a real valuation floor. Neutron is what the premium over that floor is paying for, and right now that premium is a large share of the price.

What the Financials Actually Say

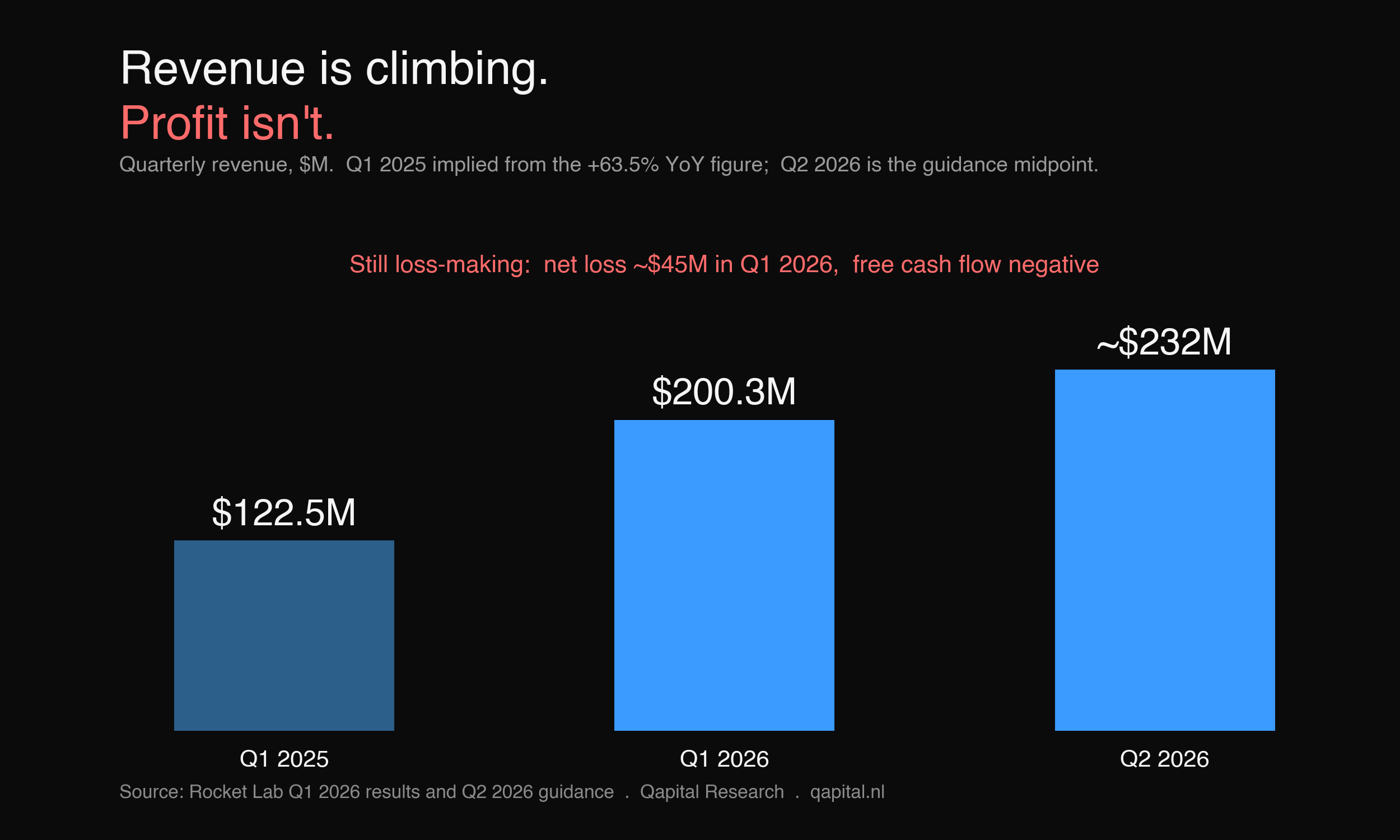

The growth is real. The profit isn’t here yet.

Q1 2026 revenue of $200.3 million beat the top of guidance. Total backlog crossed $2 billion. GAAP gross margin reached 38.2%, non-GAAP gross margin 43%, both improving. Management guided Q2 to $225 to $240 million, implying continued acceleration. Trailing-twelve-month revenue is around $680 million, growing in the mid-40s percent, and the sell side models roughly 50% forward growth.

Now the other side of the ledger. Rocket Lab posted a net loss of about $45 million in the quarter. It’s narrowing, but it’s still a loss, and free cash flow is negative while the company funds the Neutron build-out. The balance sheet is the cushion: cash and securities of roughly $1.48 billion, up sharply from about $829 million at the end of 2025, because the company raised capital. That funds the strategy. It also dilutes you.

Strip it down and the picture is clear: a fast-growing, well-capitalized, pre-profit company with an improving but still-modest margin profile, spending heavily ahead of a binary catalyst. That’s a venture-stage risk profile wearing a $66 billion market cap.

The Competition Picture

The uncomfortable truth for the “next SpaceX” thesis is that the actual SpaceX is the competition, and it isn’t close.

In launch, SpaceX dominates global orbital mass to a degree with no historical precedent, and Starship is aimed at making heavy launch radically cheaper still. Rocket Lab doesn’t compete with that and isn’t trying to. Its lane is small-lift today and medium-lift tomorrow, where the real rivals are Firefly, the legacy providers, and a field of well-funded newcomers. Neutron has to win share in a market the leader can flood with capacity at will.

Where Rocket Lab’s position is genuinely strong is the part of the business the narrative ignores: Space Systems and components. Being a trusted, vertically integrated supplier of spacecraft and subsystems to NASA, the Space Force, and commercial operators is a real, defensible position with a defense tailwind behind it. The moat, to the extent one exists today, is in the satellites, not the rockets.

So the investment question is inverted from the story everyone tells. The bull narrative is about beating SpaceX at launch, which is precisely where Rocket Lab is weakest. The durable value is in the part nobody is talking about.

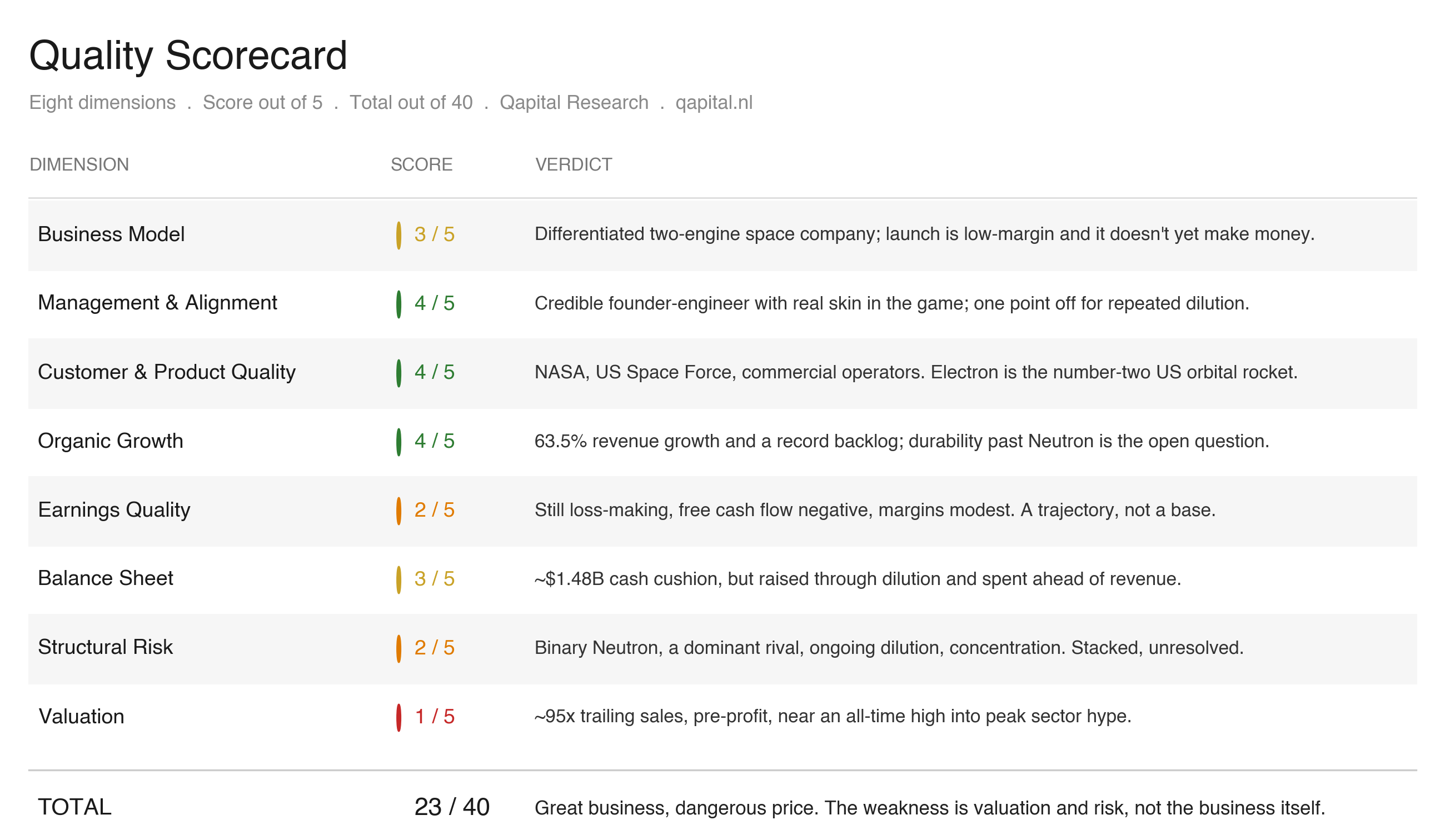

Quality Assessment

Business Model: 3/5

A genuinely differentiated, vertically integrated space company with two engines and a sensible strategy to move up the stack. Held back by the fact that launch is structurally hard and low-margin, Space Systems is good but not yet dominant, and the whole thing doesn’t yet make money.

Management and Alignment: 4/5

Peter Beck is a credible founder-engineer with real skin in the game and a strategy visibly working in the revenue mix. One point off for repeated dilution as the funding mechanism.

Customer and Product Quality: 4/5

NASA, the US Space Force, and commercial constellation operators. Electron is the number-two US orbital rocket. HASTE rides the hypersonics budget. Strong, diversified, government-anchored demand.

Organic Growth: 4/5

63.5% revenue growth, a record backlog, and contract momentum that is mostly organic. The growth is not in doubt. Its durability past Neutron is.

Earnings Quality: 2/5

Still loss-making, with negative free cash flow and improving but modest gross margins. There’s no earnings base to assess yet, only a trajectory.

Balance Sheet: 3/5

About $1.48 billion in cash and securities is a solid cushion, but it was raised through dilution and is being spent ahead of revenue. Adequate for the plan, not a fortress.

Structural Risk: 2/5

Binary Neutron execution, a leader that dominates the core market, ongoing dilution, program and customer concentration, and a valuation that assumes near-flawless delivery. Multiple, stacked, unresolved risks.

Valuation: 1/5

Roughly 95x trailing sales, pre-profit, only days off an all-time high and barely dented by a 22% pullback, into the single largest burst of sector hype on record. The weakest part of the case by a wide margin.

Total: 23 / 40

Read plainly: a good-to-strong business attached to a poor risk-adjusted setup at this price. The quality sits in the operations, in management, customers, and organic growth. The weakness sits almost entirely in valuation, earnings maturity, and stacked execution risk. Those are price-and-timing problems, not business problems, which is exactly why the rating is HOLD rather than avoid.

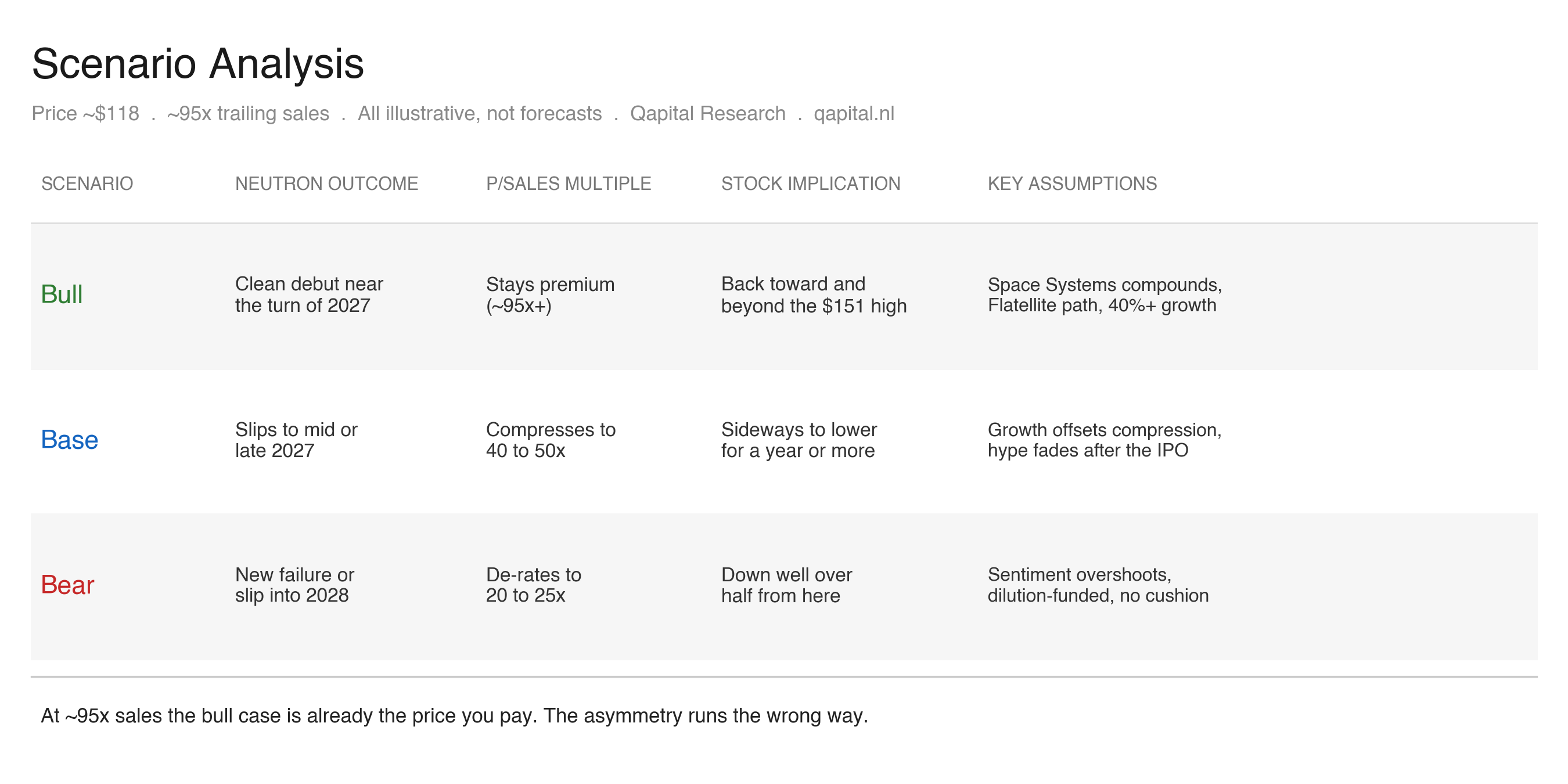

What the Numbers Say About Price

With no earnings, the honest anchor is revenue multiples and the Neutron outcome. (Net cash of ~$1.48 billion trims the figure only marginally: on enterprise value the multiple is still in the low-90s, and the cash is being spent too fast to change the picture.) Three scenarios.

Bull case. Neutron debuts cleanly around the turn of 2027 and ramps without a major failure. Space Systems keeps compounding, Flatellite opens a constellation-services path, and revenue grows north of 40% for several years. The market keeps paying a premium multiple for the only investable Western pure-play, and the stock pushes back toward and beyond its highs. This is the scenario the current price already assumes.

Base case. Neutron slips, as first launches usually do, into mid or late 2027. The business keeps growing 40-plus percent and executes well, but the sector hype cools once SpaceX actually trades and the novelty fades. The sales multiple compresses from ~95x toward the still-rich premium a high-growth, improving-margin business like this actually supports, say 40 to 50x. History sets the bar around there: high-growth, pre-profit industrials rarely hold multiples north of 40 to 50x sales once a hype cycle passes, however good the underlying business. Growth and multiple compression roughly cancel, and the stock churns sideways to lower for a year or more despite a genuinely improving business. Growth without re-rating.

Bear case. Neutron suffers another failure or a hard slip into 2028, or the post-IPO sector spike reverses the way momentum-driven spikes do, taking the most expensive, most hype-driven names down hardest. A pre-profit company funded by dilution re-rates toward 20 to 25x sales. That is not a fair-value estimate for Space Systems, which on its own would warrant a real premium; it is what a just-disappointed, dilution-funded name trades at when sentiment overshoots to the downside, as it reliably does. The result is a decline of well over half from current levels, with no earnings to cushion the fall. This is the scenario that ends the thesis at this price.

The point isn’t which scenario is correct. We can’t know that. It’s that even after a ~22% pullback from the May 27 high, at ~95x sales the bull case is already largely the price you pay today, while the base and bear cases carry materially more downside than the bull case offers upside from here. The asymmetry runs the wrong way. That is a statement about the price, not a forecast of the stock.

The Bold Call

Rocket Lab is a good company. It’s founder-led, it’s growing fast, it has a real and improving Space Systems franchise, and it owns the one seat retail investors have wanted: a Western, end-to-end space business they can actually buy. None of that is in dispute.

The problem is the price and the moment. The stock has already seen its first meaningful pullback, down roughly 22% from its May 27 high of $151 to about $118, yet even after that slide it trades at roughly 95 times trailing sales, with no profit, funded by dilution, resting on a Neutron debut that has already slipped once on a ruptured tank, in the same week the largest IPO in history comes to market. The high is nearly two weeks behind it; the enthusiasm is not. Every one of those facts is the same dynamic we wrote about in our companion note on the SpaceX listing: a price set by enthusiasm and substitution flows rather than by the cash the business produces.

The behavioral discipline writes the conclusion. You do not buy the only available substitute for SpaceX near a euphoric peak, during peak SpaceX euphoria, on a binary catalyst, and call it analysis. You put a genuinely interesting business on the watchlist and you wait for the one thing hype never hands you: a better price.

Our rating: HOLD. A great business is not the same as a good investment. The gap between them is the multiple.

The thesis changes on one of two things: a successful, on-time Neutron debut that de-risks the medium-lift franchise, or a sector-wide pullback that resets the valuation toward the high-growth-but-pre-profit reality of the business. Either one, and Rocket Lab becomes a name worth owning rather than a theme worth chasing. Both at once would be the buy of the cycle.

Being allowed to buy the space theme is not the same as being early to it. Write the trigger price. Then wait.

Sources and Disclosures

This article is research and analysis, not financial advice. Qapital Research holds no position in Rocket Lab at time of publication.

Primary sources: Rocket Lab Q1 2026 earnings release and 8-K (filed May 7, 2026, SEC EDGAR); Rocket Lab Q1 2026 earnings call transcript; Rocket Lab Q4 2025 results and backlog disclosures; FAA Neutron launch-permit filings; company commentary on the January 21 propellant-tank test anomaly.

Secondary sources: sell-side notes (Stifel price-target revision); industry reporting on the Neutron timeline and Q1 2026 contract activity; market-data providers for price, market capitalization, and 52-week range as of early June 2026.

Note on figures: Revenue, backlog, margin, cash, and net-loss figures are from Q1 2026 results. Price and market-capitalization figures are approximate, as of early June 2026, and will move. The Neutron timeline reflects guidance at the time of writing and is subject to change.

Qapital Research

Published June 2026