Micron Technology: The Memory Company That Isn't One Anymore

Ticker: NASDAQ: MU Market Cap: ~$1 trillion 52-Week Range:~$155 — ~$917 Q3 FY2026 Gross Margin Guidance: ~81%

The Number That Breaks the Model

In FY2023, Micron Technology reported revenue of $15.54 billion, down 49% year-over-year. The company posted a net loss of $5.83 billion. Every analyst who covers the memory sector had seen this movie before: commodity prices collapse, utilization rates fall, manufacturers bleed cash until the cycle turns.

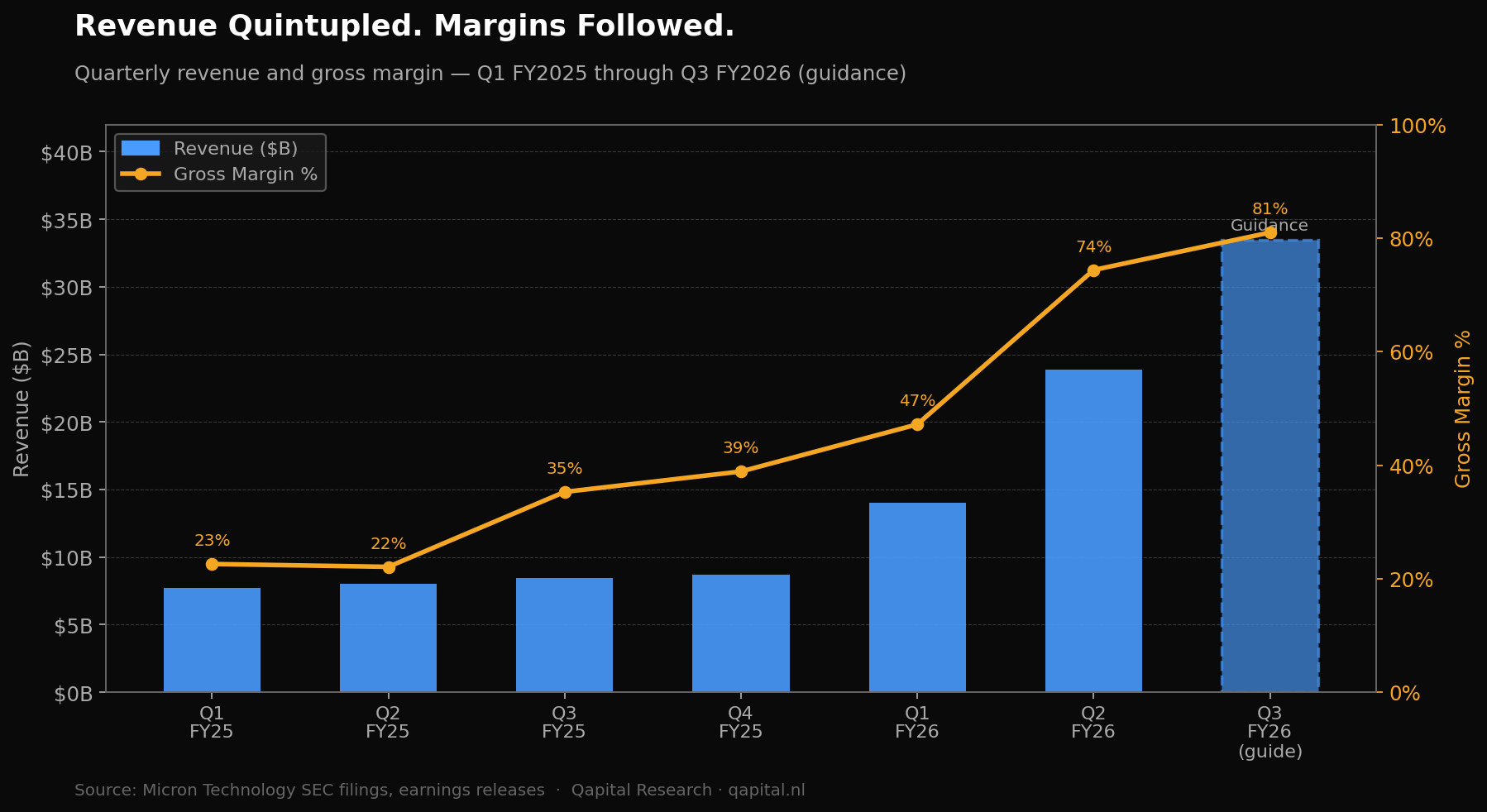

Three years later, Micron guided Q3 FY2026 revenue at $33.5 billion with gross margins of approximately 81%.

That is not a recovery. A recovery returns a business to where it was. What Micron described is a different business operating in a different market at economics that commodity memory has never produced. The question is whether the market is pricing the old company or the new one, and whether it understands why they are not the same.

The behavioral trap has a name. We will get there.

The Commodity Label

Memory semiconductors have been a commodity business for most of their commercial history. Prices are set at the spot market. Margins cycle between exceptional and deeply negative depending on supply and demand dynamics that no individual manufacturer controls. The three dominant producers, SK Hynix, Samsung, and Micron, have all lost billions in the same downturn years, all recovered in the same upturn years, and all done it again.

That pattern has produced a specific mental model in the investor community. When you hear “memory company,” you hear: cyclical, capital-intensive, no pricing power, margin collapse every three to five years. The model is accurate for commodity DRAM. It is not accurate for High Bandwidth Memory.

HBM is not priced at the spot market. It is not sold to distributors. It is not subject to the same oversupply dynamics that drive commodity DRAM pricing. HBM is sold under long-term fixed-price supply agreements directly to the hyperscale customers who embed it into AI accelerators: Nvidia’s H200, Nvidia’s Blackwell B200, AMD’s Instinct MI350X. The customers design HBM into the chip at the silicon level. Once designed in, switching memory suppliers requires significant architectural re-qualification work. Nvidia already multi-sources across all three suppliers where it can, and future architectures will be designed with greater supplier flexibility in mind. The barrier is not permanent lock-in. It is high switching friction: qualification timelines measured in quarters, not days. That friction gives Micron extended revenue visibility once a design win is secured.

This is the behavioral trap: the market applies the commodity DRAM mental model (oversupply cycles, spot-market pricing, margin collapse) to a product that operates under fixed-price multi-year contracts in a three-supplier oligopoly where the buyer cannot switch suppliers without redesigning their chip.

The two products share a factory floor, wafer-level cost pressures, and sensitivity to memory-node scaling. The pricing mechanism, contract structure, customer relationship, and switching economics have nothing in common.

The bears who keep expecting Micron’s margins to revert to the historical 40-50% range are right about commodity DRAM. The specific error is anchoring on historical margin ceilings that do not apply to the marginal dollar of Micron’s current revenue. HBM has never been priced as a commodity. It does not have a commodity margin ceiling. That gap between the label the market applies and the product that is actually generating the earnings is where this article lives.

Mehrotra and the Transformation He Built

Sanjay Mehrotra co-founded SanDisk in 1988 and ran it for 28 years before it was acquired by Western Digital for $19 billion in 2016. He joined Micron as CEO in 2017, when the company was coming out of its previous trough and beginning to build what would become its HBM franchise.

The strategic bet Mehrotra made was not obvious at the time. He redirected significant R&D investment toward HBM at a moment when commodity DRAM was still generating acceptable returns and AI accelerator demand was years from materializing at scale. The capital allocation decision to build HBM manufacturing infrastructure before the demand curve arrived is the primary reason Micron has any meaningful HBM market share today.

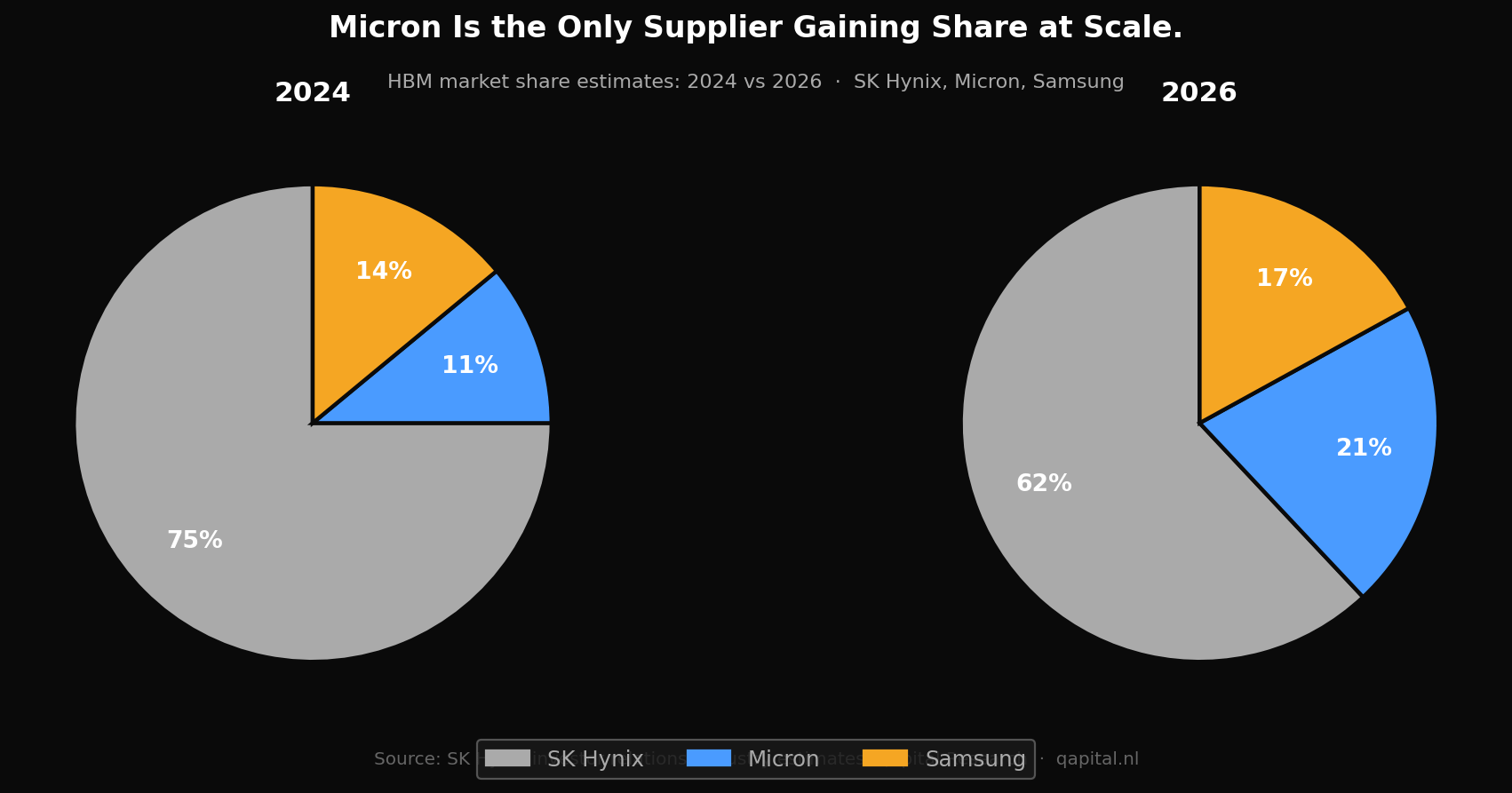

Industry estimates place Micron’s HBM share at approximately 11% in 2024, growing to around 21% in 2026. SK Hynix leads at roughly 62%, Samsung sits at approximately 17%. These figures are not disclosed audited values; they reflect analyst estimates and company commentary. The trajectory, however, is consistent across sources: Micron is the only supplier gaining share at scale.

The technical reason is documented. Micron has promoted HBM3E configurations capable of up to 9.6 gigabits per second per pin, above earlier publicly disclosed SK Hynix HBM3E specifications. Bandwidth density specifications evolve with each product generation and stack configuration, so exact comparisons shift. What does not shift: Micron’s HBM is qualified and shipping in Nvidia’s highest-margin data center products, which is the market’s revealed preference.

A note on insider ownership: $36 million in CEO share sales over six months has appeared repeatedly in bearish commentary about Micron. The Form 4 filings show every sale was executed under pre-arranged 10b5-1 trading plans, the standard mechanism executives use for planned portfolio diversification. Following the sales, Mehrotra directly holds 464,000 shares and indirectly holds 607,075 shares through grantor-retained annuity trusts. At current prices, that is approximately $1 billion in total exposure. The insider-selling thesis appears materially weakened by the retained ownership exposure.

How the HBM Machine Works

Standard DRAM is manufactured in large volumes, sold through distribution channels, and priced daily at market rates. When too much supply enters the market, prices collapse. When demand spikes, prices rise. Manufacturers cannot control which direction the cycle runs.

HBM is manufactured against a design win. Micron does not produce HBM4 and then find buyers. Nvidia and AMD lock in supply agreements at the chip design stage, specifying volumes and pricing for 12 to 24 months. Micron has indicated its 2026 HBM output is substantially committed under customer agreements entered before the year began.

The economics of a design win flow through to the income statement in a way commodity memory never does. There is no spot-market exposure. There is no inventory risk on unsold product. There is a fixed schedule of deliveries at a fixed price against a fixed customer forecast. For the period covered by the contract, Micron operates more like an aerospace supplier than a commodity manufacturer.

Those contracts remove spot-price volatility. They do not eliminate demand cyclicality: they shift where it expresses itself. If AI accelerator orders slow in 2027, the impact arrives at contract renewal, not in the daily spot market. That is a structural improvement in earnings predictability. It is not immunity from the cycle.

The capital intensity remains high. HBM manufacturing requires Through Silicon Via technology: stacking multiple DRAM dies with vertical copper connections at a pitch that commodity DRAM tooling cannot produce. The per-unit cost of HBM is substantially higher than standard DRAM; the per-unit price is higher by a wider margin. That spread is where the 81% gross margin lives.

Micron’s AXON equivalent is the relationship with Nvidia. Nvidia’s Blackwell architecture requires HBM embedded at the package level. There is no Blackwell B200 without HBM. There is no alternative supply of sufficient bandwidth at sufficient density from a fourth supplier that does not exist. Micron, SK Hynix, and Samsung are the only manufacturers in the world who can produce HBM at volume. Industry reporting indicates each supplier’s 2026 HBM allocation is substantially committed.

The Competition Picture

The three HBM suppliers are competitors and, in a structural sense, partners in maintaining the oligopoly that makes the economics possible.

SK Hynix holds approximately 62% of HBM market share and was first to qualify HBM3E with Nvidia at scale. The head start is real. SK Hynix is the default supplier for the highest-volume Nvidia GPU configurations and will be difficult to displace from that position quickly.

Samsung holds approximately 17% and has had documented qualification challenges with Nvidia. Industry reports throughout 2025 indicated Samsung faced qualification and yield challenges with Nvidia-related HBM programs, which contributed to their share loss. Samsung is addressing the technical issues and has announced a 50% HBM capacity expansion for 2026. Whether they execute the expansion on schedule and at the quality level Nvidia requires is the central uncertainty in the competitive picture.

For Micron, the Samsung execution question matters both ways. If Samsung ramps capacity and clears qualification, the oligopoly adds effective supply and price pressure becomes real. If Samsung continues to struggle with quality while ramping capacity, the effective supply increase is smaller and Micron’s share gains continue.

The risk is not only Samsung. SK Hynix holds 62% market share and will not cede it without a response. If Micron continues gaining share, SK Hynix has the financial capacity and the Nvidia relationship to compete aggressively on pricing, specification, and co-development timelines. The more important concern is coordinated over-expansion: if all three suppliers ramp capacity simultaneously on the expectation of a $100 billion TAM, and the TAM arrives later or smaller than projected, the result looks like every previous memory cycle. Semiconductor oligopolies have historically failed to maintain capacity discipline at anomalous margins. The structural argument says HBM is different. The historical argument says it usually isn’t.

On standard DRAM and NAND, Google, Amazon, and other hyperscalers are large buyers who run competitive procurement processes. Pricing pressure on the commodity segments is constant. But the commodity segments are not driving the current earnings story. HBM is. The margin profile of Micron’s business has bifurcated: commodity memory operates at historical norms while HBM produces the economics that are setting the headline numbers.

China is a limited exposure. Following the Commerce Department ban on advanced memory exports in May 2023, Micron’s China revenue fell from approximately 25% of total to approximately 7%. The remaining exposure is mostly commodity products not subject to the ban. Geopolitical risk on the high-margin HBM business is minimal. Nvidia cannot sell its AI accelerators into China either, so the HBM demand from that channel was never part of the growth thesis.

What the Financials Actually Say

Micron’s Q2 FY2026 numbers were not good. They were extraordinary.

Revenue came in at $23.86 billion, up 196% year-over-year. GAAP gross margin was 74.4%. Net income was $13.785 billion. Free cash flow was $6.899 billion, a single-quarter record. EPS of $12.07 beat consensus by a wide margin.

Q3 FY2026 guidance: $33.5 billion in revenue, plus or minus $750 million. Gross margin approximately 81%. EPS guidance approximately $19.15.

The 81% figure deserves one honest note. Constrained-supply environments in semiconductors can produce margins that overshoot the structural steady-state. Micron is currently the beneficiary of limited HBM supply against surging AI accelerator demand. As Samsung capacity comes online and all three suppliers scale, the equilibrium margin will be lower than 81%. The question is whether it settles toward 65% or toward 45%. The former is a structurally excellent business at a reasonable multiple. The latter is a cycle that looks different until it doesn’t.

At the current price of approximately $900, Micron trades at roughly 12x the annualized run rate of its Q3 guided earnings. Semiconductor investors will recognize that peak-cycle earnings frequently produce deceptively low forward multiples. The question is not whether 12x is expensive relative to current earnings. It is whether current earnings represent a structural floor or a supply-constrained peak. A standard DRAM company at cycle peak might trade at 8-10x and deserve it, because those earnings will not persist. The HBM case is that they will persist at a structurally higher level, even if not at 81% margins.

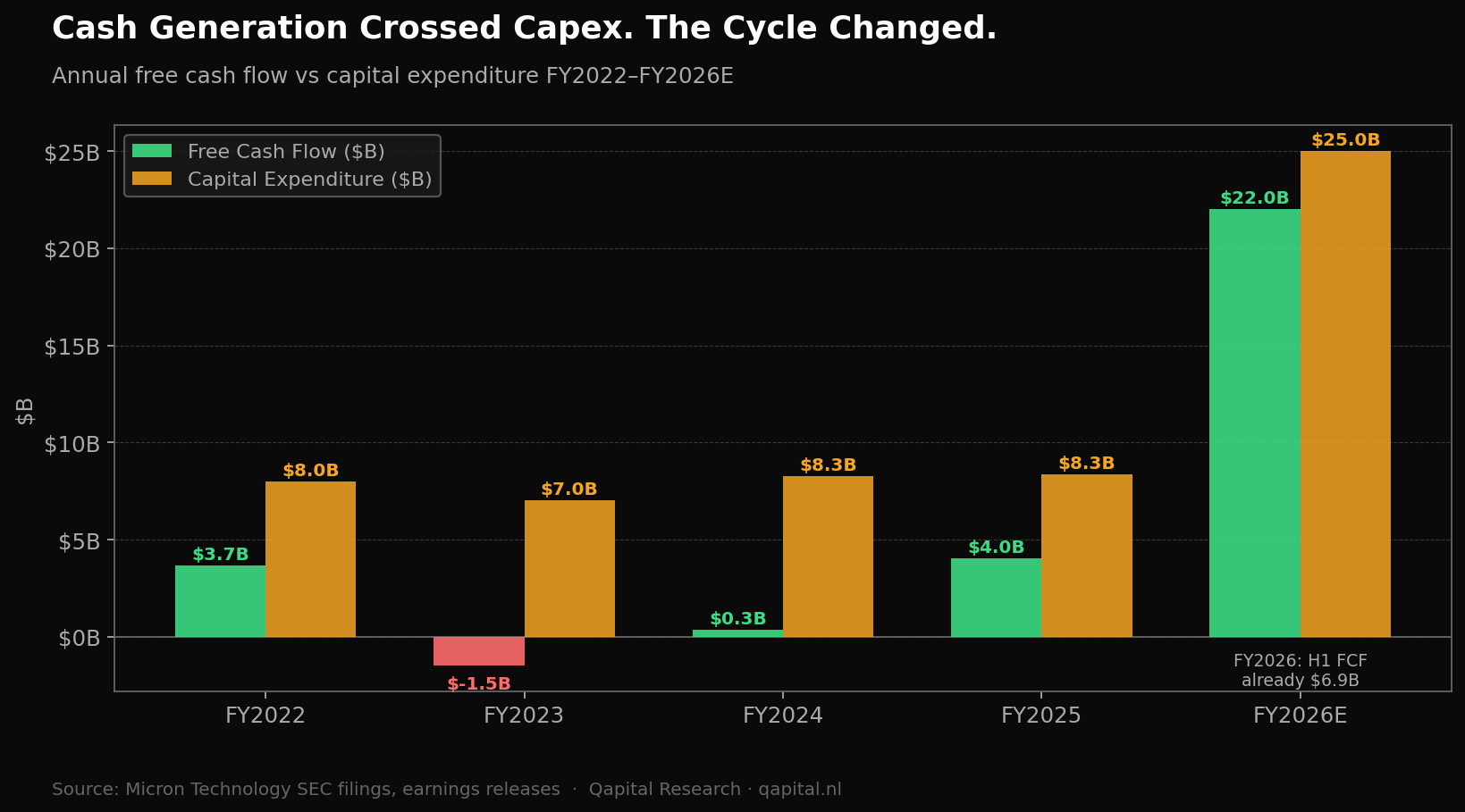

The capital expenditure picture deserves direct treatment. Micron has committed to over $25 billion in capital expenditure for FY2026. That is a large number. It reflects both the ongoing investment required to maintain HBM manufacturing capacity and the approximately $6.44 billion in CHIPS Act support the company has been awarded for US domestic manufacturing. That figure combines direct grants, federally subsidized loans, and investment tax incentives. Not all of it is direct cash. Micron received $2.256 billion of that total in the first half of FY2026. The capex is high, but it is not uneconomic: the company generated $6.899 billion in free cash flow in a single quarter while running that capex level.

Net cash and marketable investments minus debt is approximately $6.5 billion. The balance sheet can support the investment cycle.

The SBC picture is cleaner than AppLovin’s covered last week. At roughly 2-3% of revenue at current run rates, it is not distorting the earnings picture materially.

One number stands above the rest: the HBM TAM that management projects growing from approximately $35 billion in 2025 to approximately $100 billion in 2028. That projection assumes sustained AI infrastructure buildout at current intensity. Any normalization in hyperscaler capex, driven by ROI skepticism, improvements in compute efficiency, or a slowdown in model scaling, would compress the TAM outlook directly. The number is derived from AI capex forecasts that are themselves extrapolations. Even with that caveat: if the TAM reaches $70 billion rather than $100 billion and Micron holds 21% share, the revenue implied still supports the capital investment and the BUY thesis.

The Bear Case, Named Directly

The bear case for Micron is not that the business is bad. It is that the current margins are historically anomalous and will normalize before the valuation adjusts.

The specific mechanism: Samsung executes its 50% HBM capacity expansion on schedule, clears Nvidia qualification, and supplies sufficient incremental volume to create pricing pressure across HBM contracts when existing agreements roll over in 2027. Under this scenario, gross margins compress from 81% toward 55-60%, earnings fall from the $76 annualized run rate implied by Q3 guidance toward something closer to $45-50, and the stock re-rates from 12x to 10x that lower earnings base, implying a price around $450-500.

That is the coherent bear case. It requires Samsung execution that has not been demonstrated at scale with Nvidia’s quality standards. It requires that HBM pricing pressure materializes faster than demand growth absorbs the new supply. And it requires the $100 billion TAM projection to miss.

The second element of the bear case involves cycle history. FY2023 is the data point every memory bear will show you: revenue down 49%, $5.83 billion net loss, a company that looked like it might not survive a prolonged down cycle. If commodity memory dynamics reassert, history shows how severe the damage can be. The counterargument is that the HBM business did not exist in FY2023 at anything approaching current scale. The $15.54 billion in FY2023 revenue was almost entirely commodity DRAM and NAND. The business that is generating 81% gross margins today is not the same business that posted that loss.

The FY2023 comparison is the most powerful argument in the bear toolkit. It is also the clearest illustration of why applying the commodity label to HBM is the wrong mental model. Those are two different businesses wearing the same ticker.

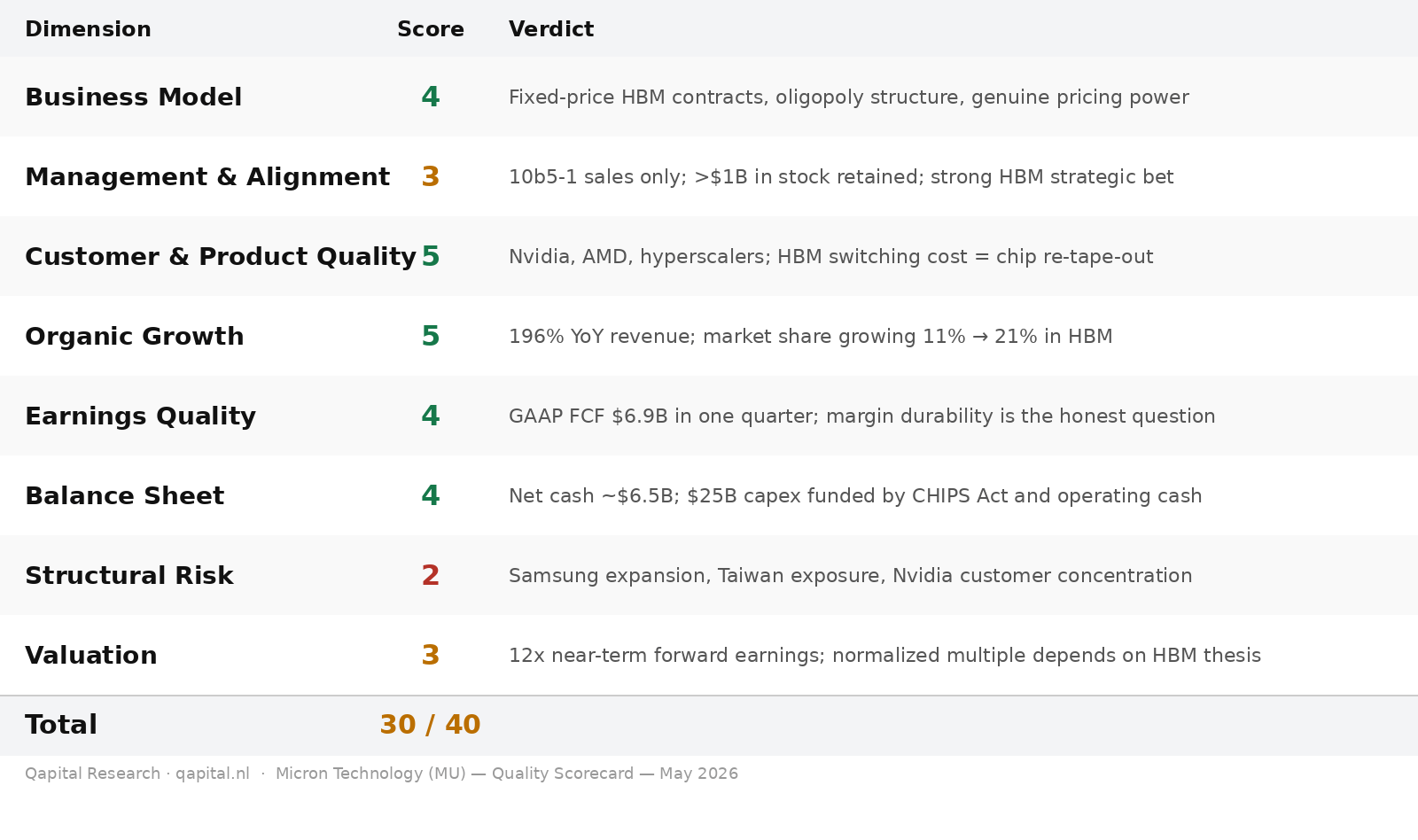

Quality Assessment

Business Model — 4/5 HBM’s fixed-price contract structure, co-packaging with AI accelerators, and three-supplier oligopoly produce real pricing power in a market segment that has never had it before. The commodity segments remain capital-intensive without the same characteristics. The split profile prevents a perfect score, but the direction of the business is clearly toward the higher-quality segment.

Management and Alignment — 3/5 Mehrotra’s strategic positioning into HBM years before demand materialized is the defining management decision of the last decade in memory semiconductors. Total beneficial ownership exceeds $1 billion at current prices. The 10b5-1 sales are routine diversification. The score is 3 rather than 4 because Micron is not founder-led in the same sense as the highest-conviction management situations, and the $25 billion capex commitment at what may be a peak moment carries execution risk.

Customer and Product Quality — 5/5 Nvidia, AMD, and the hyperscale cloud providers. HBM designed into silicon with multi-year switching costs. The customer concentration in AI accelerator demand is real, but the customers are the least likely to disappear. Full marks.

Organic Growth — 5/5 Revenue up 196% year-over-year. Market share growing from 11% to 21% in HBM. This is not financial engineering or acquisition. The growth is organic and the pipeline visibility (2026 HBM4 sold out) extends it at least through the year. Full marks.

Earnings Quality — 4/5 FCF of $6.899 billion in a single quarter, GAAP gross margins of 74.4%, no significant adjustments distorting the headline. The one honest note: the margins are historically unprecedented for any memory company at any scale. Durability depends on the HBM contract thesis holding. That uncertainty costs one point.

Balance Sheet — 4/5 Net cash of approximately $6.5 billion with $2.256 billion in CHIPS Act grants received. The $25 billion capex commitment is substantial but manageable against current cash generation. Not a fortress balance sheet, but not a concern at current earnings rates.

Structural Risk — 2/5 Three risks that are not fully resolved. First, Samsung’s HBM capacity expansion: if they execute, supply and pricing dynamics change in 2027. Second, geopolitical exposure: Micron manufactures in Taiwan and Japan alongside US operations, and a Taiwan Strait scenario produces supply chain disruption that no hedge addresses. Third, customer concentration: Nvidia’s AI accelerator trajectory is the underlying driver of HBM demand. A Nvidia-specific event, such as a competitor closing the gap or a hyperscaler shifting architecture, would transmit directly to Micron’s revenue. The structural risks are real and multi-layered.

Valuation — 3/5 At approximately 12x near-term forward earnings, the stock is not expensive relative to the current earnings trajectory. On normalized earnings, assuming margin compression from 81% toward 60% as the cycle plays out, the forward multiple expands materially. The valuation is reasonable if the structural thesis holds; it is not cheap if it does not. A 3 reflects that honest ambiguity.

Total: 30 / 40

What the Numbers Say About Price

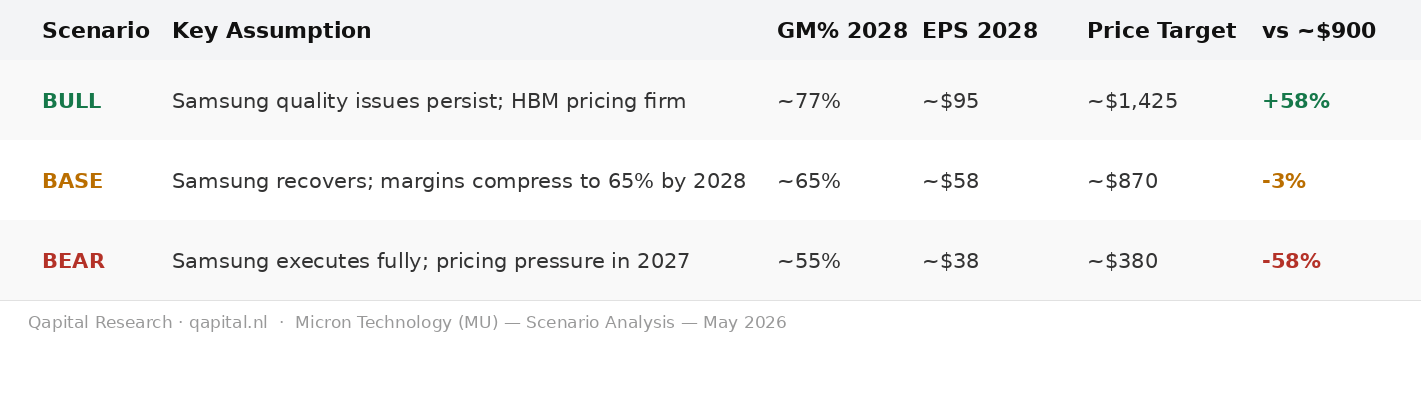

Three scenarios, each built on an explicit assumption about what happens to HBM margins as Samsung capacity comes online.

Base case: Gross margins compress gradually from 81% toward 65% over 2027-2028 as Samsung recovers quality and adds supply. Revenue continues growing as HBM TAM expands toward $100 billion. Micron maintains approximately 22% market share. Earnings stabilize around $55-60 annualized by 2028. At 15x earnings, a premium to historical memory multiples reflecting the structural change, equity value per share approaches $825-900. Current price is approximately $900. The base case says you are roughly fairly valued with upside if TAM growth outpaces supply expansion.

Bull case: Samsung fails to clear Nvidia qualification at the required quality level through 2027. HBM pricing holds above 75% gross margins. TAM hits $100 billion by 2028 on schedule. Micron grows share to 25%. Annualized earnings approach $90-100. At 15x, equity value per share approaches $1,350-1,500. Roughly in line with UBS’s $1,625 target on slightly more aggressive assumptions.

Bear case: Samsung executes capacity expansion, pricing pressure materializes in 2027 contract negotiations. Gross margins compress to 55%. Revenue growth slows as commodity segments face another trough. Annualized earnings fall toward $35-40. At 10x on a business that looks cyclical again, equity value approaches $350-400. This is the scenario that ends the thesis.

The probability weighting that produces the current price is approximately: base case 50%, bull case 30%, bear case 20%. That distribution implies the market is assigning roughly one-in-five odds to the full reversion scenario, consistent with a stock that has moved from $155 to $900 in twelve months and where the bear thesis remains intellectually coherent even if it is not the central case.

There is a fourth scenario not captured in the three above: architectural shift. If AI accelerators migrate toward memory-on-package alternatives or new interconnect paradigms that reduce HBM dependency, the TAM projection changes regardless of Samsung’s execution. Current Nvidia, AMD, and hyperscaler roadmaps all assume HBM through at least 2028, making this a low-probability event over any 24-month horizon. It does not change the rating. It belongs in the model.

The Bold Call

Micron Technology’s business has not peaked. The Q3 FY2026 guidance implies something the market may still be underweighting: this is not a company running at full utilization waiting for the cycle to turn. This is a company selling its highest-margin product under fixed-price contracts that were signed before the year began, delivering to customers who cannot switch suppliers without redesigning their chip, in a market growing from $35 billion to an estimated $100 billion in three years.

The structural argument is not “this time is different” as a hand-wave. It is a specific claim about a specific product: HBM operates under contract economics that commodity DRAM never had and will never have, because AI accelerator manufacturers cannot afford the supply uncertainty that spot-market procurement would create.

The risks are real and they deserve naming. Samsung’s capacity expansion is the central variable. A Taiwan Strait scenario is not zero probability. Customer concentration in Nvidia is a real dependency. The $25 billion capex commitment is a bet on sustained demand that the company cannot reverse easily. The FY2023 data point will not go away. Memory companies can lose $5 billion in a year.

What is also real: CEO Sanjay Mehrotra holds over $1 billion in Micron equity. The order book for 2026 is fully committed. The technical specification lead over SK Hynix is documented and shipping in Nvidia’s flagship products. The CHIPS Act tailwind reduces capex burden. And the bear case requires Samsung to succeed where it has recently failed.

Our rating: BUY.

The price at which this thesis changes is a confirmed Samsung HBM qualification at Nvidia scale and evidence of pricing pressure in early 2027 contract negotiations. If those two signals arrive together, revisit.

The commodity label is the wrong label. Strip it off.

Sources and Disclosures

This article is research and analysis, not financial advice. Qapital Research holds no position in Micron Technology at time of publication.

Primary sources: Micron Technology Q2 FY2026 earnings release (March 2026); Micron Technology Q2 FY2026 10-Q filed with the SEC; Micron Technology Q3 FY2026 guidance call transcript; Micron Technology Form 4 insider trading filings (SEC EDGAR); CHIPS and Science Act award documentation.

Secondary sources: SK Hynix investor relations (HBM market share data); AMD Instinct MI350X product specifications; industry analyst HBM TAM projections cited as management commentary from earnings calls.

Disclosures: The SEC has not raised any concerns about Micron’s financial reporting. No regulatory investigations or informal inquiries affecting Micron are disclosed in their public filings as of time of writing.